|

My morning routine isn’t guru approved – and that’s what makes it perfect for me

God, can we please stop with guilting people over the morning pages, the journaling, the meditation, the drinking 18 gallons of mint-infused water, and the yoga? If you want to do those, GREAT! But you don’t have to. My rules for the perfect morning:

Why we take bad advice about morning routinesThere’s a new cottage industry of people telling you all the thing you “should†do every morning. But as it gets more absurdly specific, it gets even more performative. Drink a glass of water? No! Make sure you infuse it with turmeric and mint. If you like mint, great. But just adding mint doesn’t do anything. The real win here is to be intentional about what you want to do — and how you want to do it. This is a lot harder than making an esoteric recommendation like drinking 6oz of yak tea. People love those recommendations because all of us want a magic bullet, or “secrets†that will magically change everything for us. Deep down, we know it’s all bullshit. I spoke to Tim Ferriss about this on his podcast a few years ago – you can watch the interview here: How to create the right morning routine for youReal happiness and productivity comes from making much deeper changes.

This is a lot harder than taking some magic pill. It means fundamentally restructuring your lifestyle, including how you work (maybe even where you work), how you relax, what time you go to sleep, and even what you think of yourself (“I’m not a morning person†is an identity you can rewrite).

Learn how to build good habits and break bad ones with my FREE Ultimate Guide to Habits.

Real morning routines are decided the week before, month before, and year beforeI love the idea of crafting a meaningful morning for your personal Rich Life. I do not love the cargo-cult fanaticism about random tactics. The best morning routine is decided the day before, the week before, and the year before by mastering the fundamentals. What I mean by this: When I wake up and have a leisurely morning, then wander over to start working, I open my calendar. What I see has been decided weeks and months before:

It’s far better to consciously decide what your morning looks like. If you want to roll over and check Instagram (as I do), that’s great. The first thing I get to read is some 17-year-old telling me I am wrong about investing. Good morning, @crypt0_4_lyfe7291. Thanks for your contributions to the investing literature. Be realistic about your time and energyLook at your calendar for tomorrow. Have you thought about how your energy fluctuates throughout the day? Does your calendar include the 3 most important things that need to get done? Is it realistic — does it include time to use the bathroom and eat and just zone out?

If you want your morning routine to stick for good, learn how to master your psychology in my free Ultimate Guide to Habits.

3 questions to ask yourself when designing your morning routine

As you tackle these questions, you may realize that your perfect morning is a lot closer than you thought. My morning routine isn’t guru approved – and that’s what makes it perfect for me is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/my-morning-routine-isnt-guru-approved.html October 05, 2021 at 01:34PM

0 Comments

Our DIY Heat Pump Install – Free Heating and Cooling for Life?

To most of the Internet, Mr. Money Mustache is known as the quirky early retirement financial guy, and this is a blog about Money. But really, I’m not a finance guy – someone who devotes most of his time to optimizing money. I’m more of a general Life Engineer – someone who tries to optimize everything that is fun and interesting in life, and money is just one of those things. Optimizing means getting the most good out of something – whether it is money, time, health or happiness, while minimizing waste. This is what allows us to make win/win decisions (for example things that make you richer and healthier and happier), rather than win/lose compromises (giving up something you actually like, just to save or earn more money) One of these win/win things for me has always been optimizing my own houses and buildings to be more comfortable and stylish, while costing less to own and maintain and heat and cool. After all, out of all possible decisions, your choice of home may have the biggest effect on both your financial and emotional wellbeing. Get a reasonable house that is close to your friends and your work, and you’re off to a great start. So anyway, this past summer all my favorite factors of optimizing, learning, effort, saving shit-tons of money and reducing loads of waste and pollution came together in the form of a DIY Heat Pump Installation on our commercial building downtown, the home of MMM HQ Coworking. Why Are Heat Pumps Super Exciting? Heat pumps are a technology that has recently jumped into prime time and are about to change everything about houses, just as the iPhone did to the tech industry about twelve years ago and just like electric cars are doing to transportation right now. The reason is that they have these fundamental advantages:

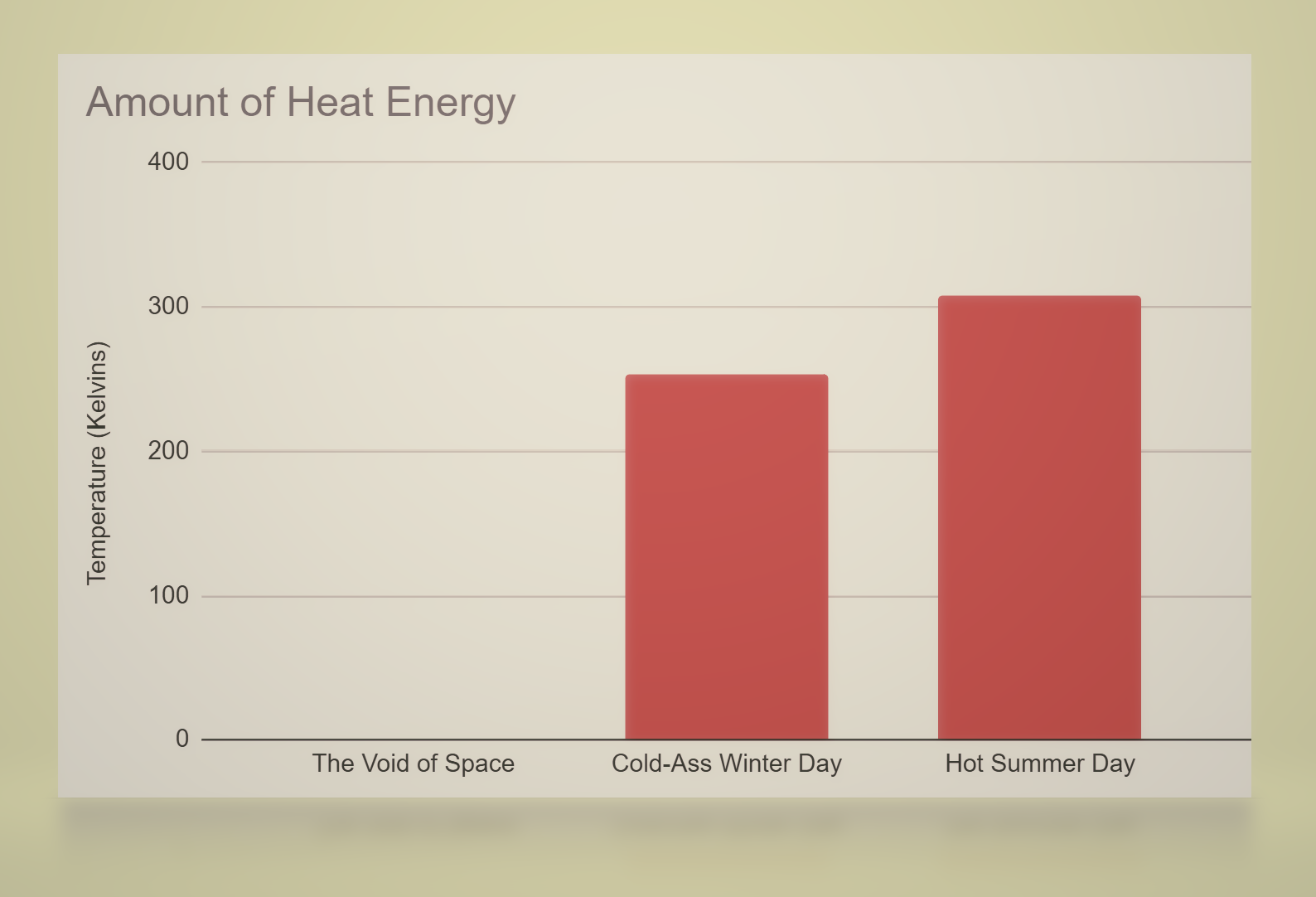

How Does a Heat Pump Magically Suck Heat Out of Cold Air? Heat pumps save money and energy because they aren’t generating heat directly like an old electric baseboard heater. They are mostly just moving heat around – from inside to outside in the summer, and from outside to inside in winter. To many people, that second situation sounds like magic, but that’s just because of our skewed perception as human beings – a creature that evolved in the warm tropics of the planet Earth. Really, there is plenty of heat even in winter air – if you view it from the Eyes of Physics:

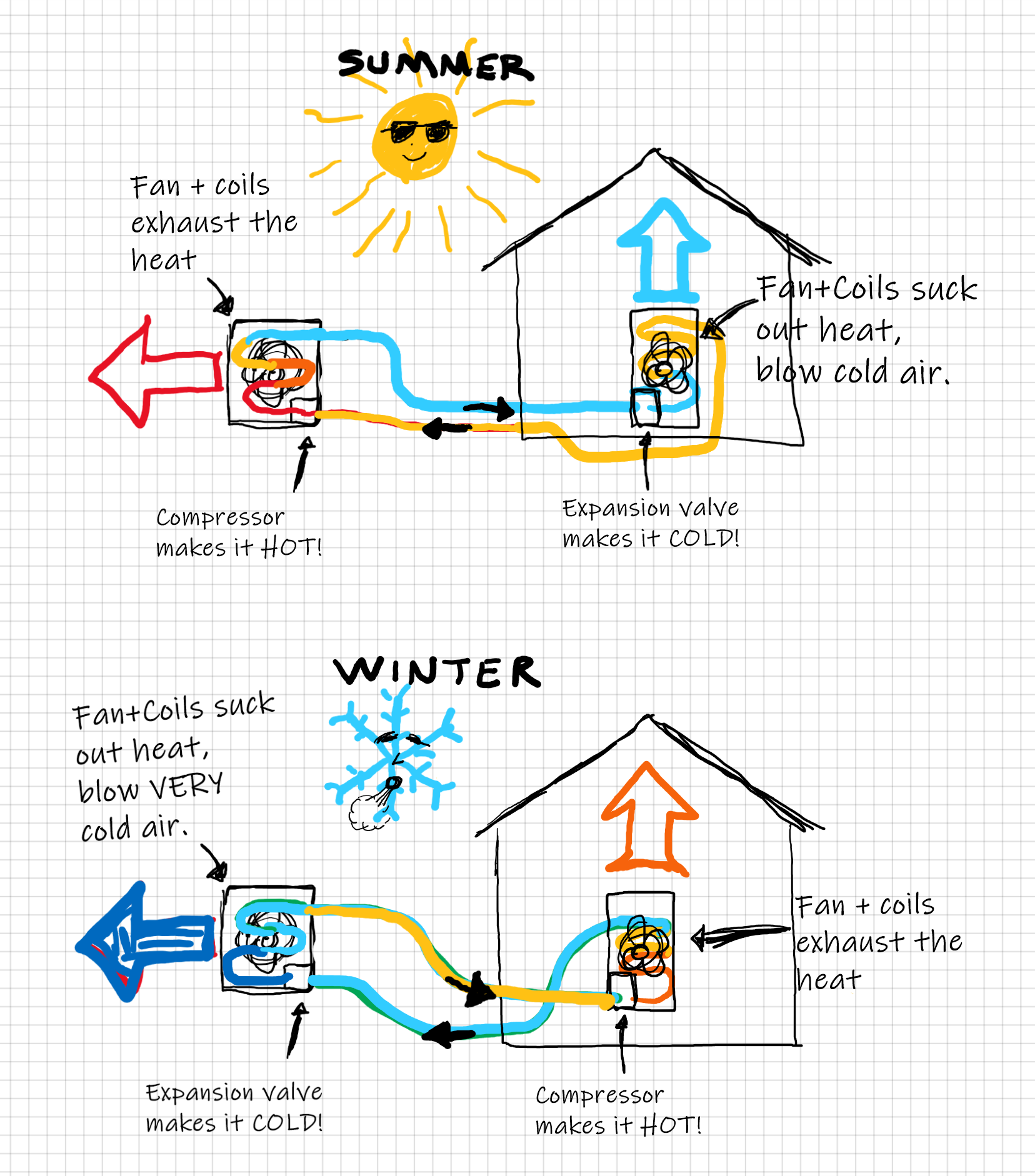

So, a modern heat pump can easily suck loads of heat even out of air that feels cold to your skin. It does it like this:

You know what else does this exact same trick? Your own FREEZER! Those things typically maintain an inside temperature of about -10F, which means that somehow it is sucking heat out of the air even at sub-zero temperatures, pumping it out to the coils underneath with a fan blowing past them. And if you put your hand there to feel that airflow, what do you feel? Warmth! Show Me The Money

Before we get into the real details, check out the quick numbers for the heat pump I just installed. Note that I live in Colorado, which has lots of heat and a moderate amount of cold – right about what you’d expect from our position halfway between Maine and California.

Annual return on investment (ROI) rate: 15% . Even better: That $275 annual figure for our electricity consumption is what we would have paid, if we had to buy all our electricity off the grid at 10 cents per kWh. But since we generate a surplus of power from our DIY solar array, our net cost is much less than that. You could even say that all of our heating and cooling is “free” on an ongoing basis, although we did spend $5000 to build the 5.5 kW solar setup in the first place. So Is A Heat Pump Really a Do-It-Yourself Project?

In a word: Yes, if you are a fairly competent do-it-yourselfer, and you choose a DIY-friendly heat pump kit. It is considerably easier than installing a gas furnace or a metal roof, but not as easy as putting together IKEA furniture. Our first install took about 16 person-hours of work for the main job (two people working a full day). Plus I spent about another sixteen dusty hours upgrading the duct work and building custom metal shapes to route the air because our coworking building was so old that the original asbestos-and-mouse-shit ducts were just not worth keeping.

The value of doing it yourself is that furnace work is one of the biggest returns on your time as a homeowner. Where I live, even a gas furnace + air conditioner replacement can cost $10,000. And although a heat pump hardware only costs about the same amount as conventional furnace+AC ($4000), the companies like to charge more for the newer stuff (or even worse, try to convince you that you’re stupid for even asking about it!). In other words, even conservatively speaking, for a basic installation you are saving about $6000 in exchange for doing that 16 hours of work, which amounts to a solid $375 per hour.

But Wait! Don’t forget about Rebates!

Even if you’re not a tinkerer, there are some good programs out there that will help subsidize the cost of an upgrade like this. The US EPA offers federal tax credits for lots of things including heat pumps, and local agencies have their own programs – for example neighboring Fort Collins will chip in $2200 towards a unit like ours, which could cover most of the cost of a professional installation! . So if you are ready to upgrade to a heat pump, you either need an honest HVAC company who will install a reasonably-priced machine for you and charge you a reasonable hourly rate. Or, you need to flex your Money Mustache Muscles on the project and do it yourself. Of course, I chose the latter approach as always, so let’s get into the details of or install! Step One: Pick a Heat Pump

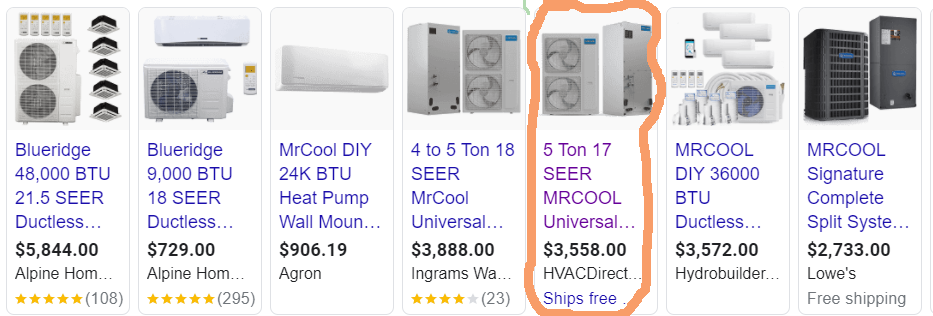

There are two things you’re looking for here: physical size and heat output. The size and shape of indoor portion (the air handler) of the new system have to be similar to your old furnace, or you need to have a plan for how to adapt the new one to blow into your old pipes. As you’ll see below, I chose to do the adapting. As for the heat output, old furnace was a “100,000 BTU” unit, which is a measure of the amount of natural gas it can suck in and burn each hour. Since it was only about 75% efficient, the heat output was about 75,000 BTU (the real units here are the archaic “British Thermal Units Per Hour”, but all you really need to know is that this is still more than enough to keep our leaky, sprawling 2400 square foot brick building warm easily through even the coldest winters.) In the most extreme situation (for us this would be a 24-hour period where the temperature is barely above 0F, and it typically does happen at least once every few years), I measured that our old furnace was running for about 8 hours per day, which means our average heat loss was about 25,000 BTU on a continuous basis (75k multiplied by ⅓ of the total hours in a day) On the cooling side, we had virtually no air conditioning. Just a few crappy portable units scattered throughout the building, with a total combined cooling power of about 20,000 BTU. This wasn’t quite enough to beat the heat in the event of a fully occupied building on a 100F day. The solution for me was thus pretty simple: the biggest Mr. Cool “Universal” combined heat/cool system, which I started conveniently seeing Google ads for everywhere once I started my research. This beauty is good for about 60,000 BTU of both heating and cooling, which could also be expressed in the even more archaic form of “5 tons”

So I bought the circled option above. In my case, I placed the order through Home Depot website, with the free “ship to store” option, but you could also try your local Lowe’s, Alpine Home Air is good, and Ingrams now sells this unit (including the required 25 ft lineset) through Amazon. Step Two: Remove your old furnace

Safety tip: Make sure you turn off both the gas and electric supply to your furnace before messing with it, as well as opening some windows and running a fan to clear out any remnants of gas as you disconnect pipes. But once you have it safely disabled, it is as simple as carefully un-wrenching, unscrewing, and cutting away parts of the old furnace (while carefully preserving your existing ductwork) until you have the old one fully removed. You can sell or give it away on Craigslist, or drop off for free at a metal recycling facility.

Step Two: adapt the ductwork as needed

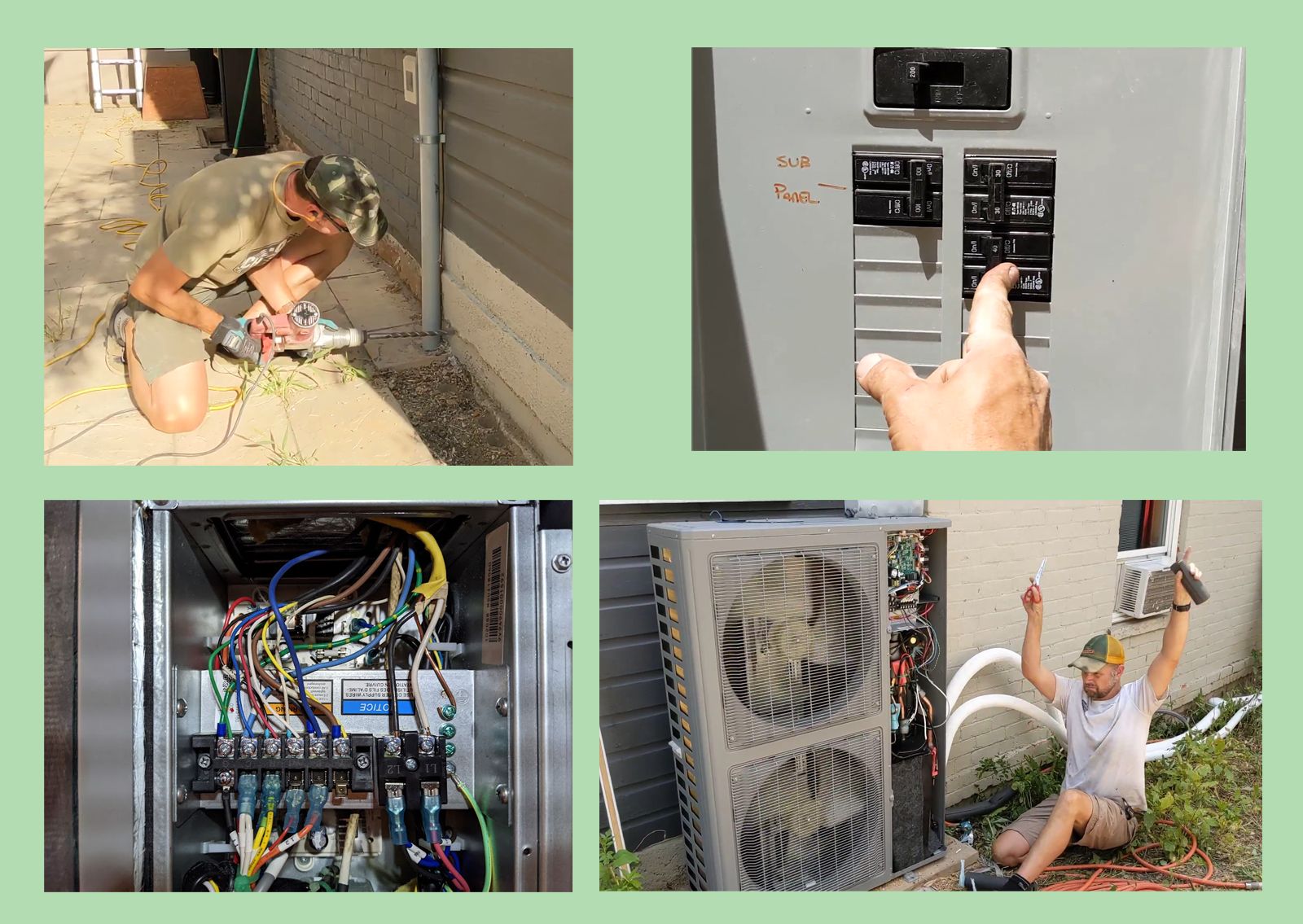

If you’re lucky (the old furnace and new heat pump are almost the same size), this step will be easy. You just connect the return ductwork to the bottom of the machine, and the supply ducts to the top. However, I was not lucky. Because our basement ceiling is so low, I had to install the heat pump horizontally (it is designed to allow this), and then build some adapters to allow the air to flow the way I needed. On top of that, most of our ducts were falling apart and poorly shaped and useless – so I repaired or replaced a bunch of them while I was in the process. This took a lot of work, but my biggest allies were a huge roll of wide, reinforced silver tape, and simple sheet metal tools like shears, angle grinder, self-piercing screws, a good breathing mask, headlamp and work gloves.

Step Three: Fit in the new heat pump

Aside from the fact that the thing is heavy (ours was around 250 pounds), this connection is surprisingly easy once you have the ducts ready. You just screw and seal the sheet metal boxes to the bottom and the top of the heat pump. And at this point, you should be getting excited because the end is in sight. Step Four: Place the Outdoor Unit Where You Want It Since the outdoor unit is another 300 pounds, you’ll want a high quality dolly and some ratcheting straps, as well as a strong friend nearby to help you wrangle it into place. Your goal is to put this thing somewhere beside your house that is out of the way, but also close to wherever you just put the air handler in the basement. Then you need a lineset that is long enough to connect them together – and shorter is generally better for both cost and performance reasons (we used a 35 footer). We put our condenser on a couple of sturdy, level concrete pads. Step Five: Run the Lineset

The lineset is a pair of flexible copper tubes that are wrapped in insulation. They are bulky, so even our 35-foot set came in a BIG roll the size of a big-screen television box. You need to carefully unroll and straighten it, and feed it in through a roughly 4” hole you drill in the side of your house so you can connect the condenser outside to the air handler unit inside. We had the added challenge of having to punch through an eight-inch-thick BRICK WALL, so I had to spend some good workout time wrestling with this massive concrete core driller, mounted to a high-torque low speed drill.

Once the lineset is in position, the connection is refreshingly easy: you carefully follow the instructions to tighten on the right nuts with a wrench, open some valves with an alan key, and you will hear the refreshing PSSSSssssssshhhhh as the refrigerant is released into the system. (This is the part that an HVAC technician would normally have to do, Mr. Cool gets around the issue by using special valves and having pre-charged linesets. More expensive, but very much worth it for the time and labor savings!) Final Step: Run the Electrical Wires

This will vary depending on the system, but ours called for the following wiring, which I subcontracted out to my partner Mr. 1500:

The Victory Lap: Fire It Up!

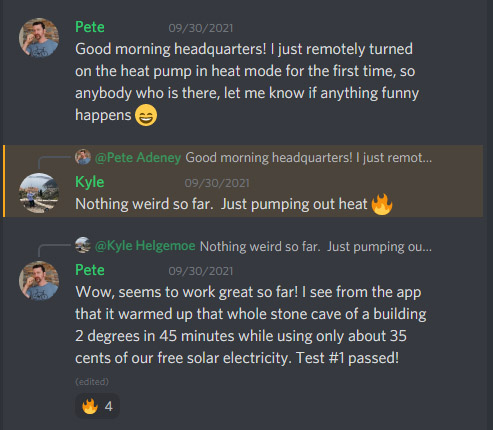

We cranked through all of these steps carefully and then flipped on the breakers with great fanfare: SUCCESS! – The Ecobee lit up and started guiding us through its setup screens. Once complete, we slid the desired temperature way down in hopes of experiencing some much-needed Air Conditioning on this hot July day. And nothing happened. We ran out to the outdoor unit and found it was just sitting there, with LEDs illuminated but nothing else happening. We both started sweating bullets. Had we made a foolish mistake and bought a faulty unit? Did we screw something up in the install? Nope – it turns out there is simply a three-minute delay between that first activation and the time Mr. Cool starts his cooling. Very slowly and with great grace, the big fan blades began to rotate, graaaaadually speeding up, with the hum of the compressor so quiet in the background that I had to press my ear up to the thing just to verify that it was really working. But boy was it ever working – we ran inside and found that that icy cold air was just blasting out of each of the seven large vents spread throughout our building, and baking hot air was now shooting out of the outdoor unit. We had instantly beat the summer heat and everybody inside raised a cheer to this new luxury. Epilogue, Three Months Later: How Well Does It Work?

Throughout the rest of the summer, we have had a lot of fun putting this system through its paces, and it has proven itself to be an incredible cooling machine. We had several events with over fifty hot bodies packed in for some of our entrepreneurship and social gatherings while outdoor temperatures were in the 90s – and we were able to maintain comfort effortlessly. The next test will of course be the winter. Here in early October, we have just turned the corner where the building has required just a bit of heat to start some mornings. With a few taps on the Ecobee phone app, I was able to flip the system over to heating mode and give it a whirl. It worked great – heating the building quickly and quietly.

But I’ll update this article over time as we move through cooler seasons. I expect it to continue to perform just great – but it will be fun to verify and reassuring to skeptics out there once we see it with our own eyes. Extra Cool Detail: How Much Electricity Does It Use?

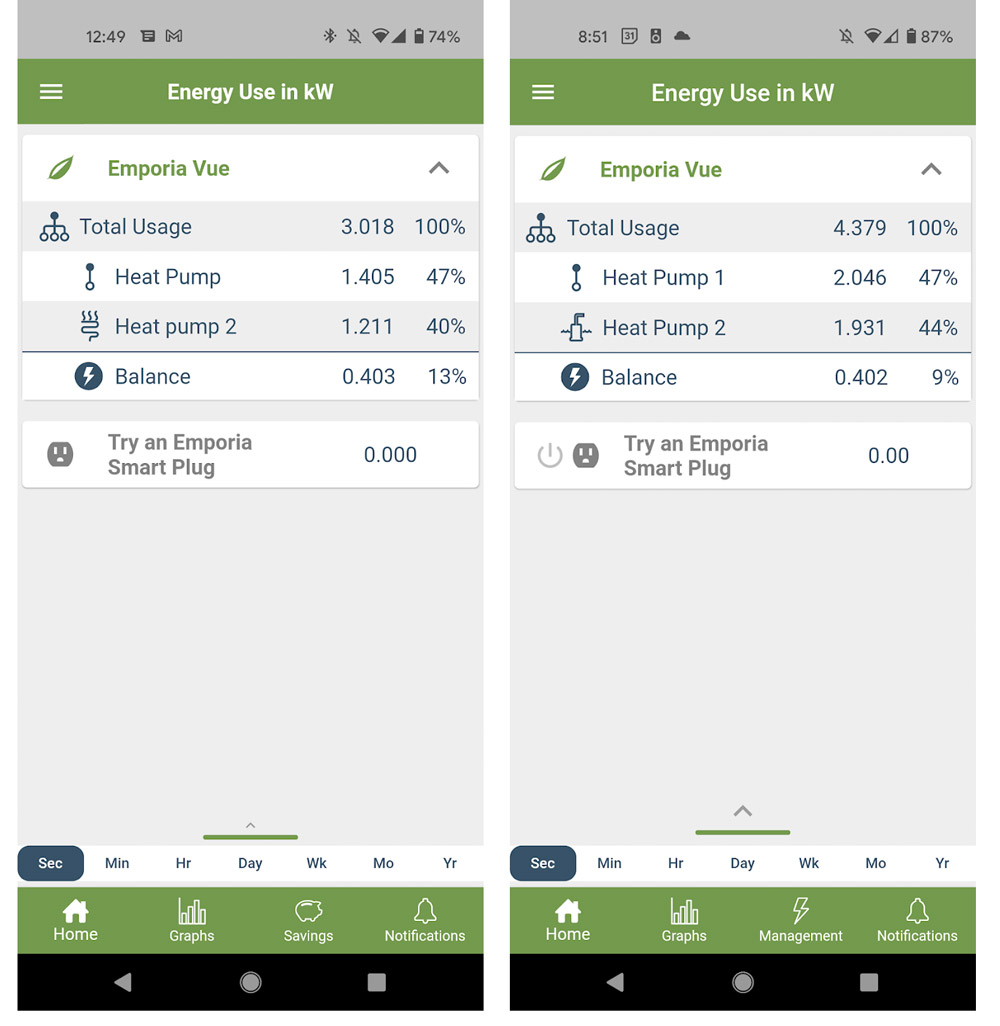

Of course, being MMM I was not content to just sit back and soak in the cool breeze of accomplishment just yet. I needed one final bit of data – a record of just how much energy this heat pump was sucking down in both heating and cooling modes, so we can get a better estimate of how much money it is saving us over the years. So I installed a system called the Emporia Energy Monitor into the circuit panel, which is currently the best value on the market for such a well-designed gadget. This allows me to track and record the full details of the energy flow – through every circuit in the house if I choose to do so. For now, I just have it watching over the heat pump. What I found is that in cooling mode, the Mr. Cool uses about 2600 watts on an ongoing basis (about the same as two large window air conditioners), which translates to 26 cents per hour of electricity. On the hottest days with the most people, I found the system ran about six hours, meaning our peak electricity use was only about $1.50 per day! To me, this was pretty remarkable – this was a 95 degree day with 50 people in the building, roughly equivalent to trying to cool a mid-sized restaurant in Texas. Yet even if we repeated this extreme situation every day, we’d rack up an air conditioning bill of only about $45.00 per month! I found that the heating mode was a bit more thirsty, with consumption at 4000 watts, or 40 cents per hour. Based on my earlier estimates of heat loss on the coldest possible days, we could be in for about 18 hours of runtime per day, which would be $7.20 of electricity. So, if the Headquarters were moved to an extremely cold climate and plunged into neverending 0F / -18C conditions for an entire month (which would make it colder than Duluth Minnesota or Ottawa Canada), we’d still face a heating bill no higher than $210 for the month. But in more realistic conditions for Colorado, we would expect about half of that level of energy consumption. And of course this is only for the month or two of our short cold season. For the rest of the year, heating is even easier. Conclusion: Heat Pumps Are The Bomb So there you have it: we dreamed about it for years, finally did it, and I could not be happier. It is such a joy to not even have an account with the gas company, and to know that this part of our expenses will be zero, forever. And of course it’s even better to know that even the electricity cost numbers in this article are just for your own comparison – in reality, we make more than enough solar electricity run this whole thing for free just from the pretty squares of black glass on the roof. Free heating and cooling for life, with no pollution (with free operation of our laptop computers and beer fridges, and free charging of our electric cars to boot) – This truly is the way of the future! In The Comments: Do you have any questions about heat pumps or other home efficiency products? And if you have a heat pump of your own, what do you think of it? Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/our-diy-heat-pump-install-free-heating.html October 05, 2021 at 10:34AM

Debt consolidation: How does it work and is it right for you?

When you have debts everywhere you turn, it can feel like you’re completely swamped. Your hands are tied every payday as you funnel money into paying off debts, leaving you with no room to save. That’s why a lot of people turn to debt consolidation, which is when you use a loan to pay off all of your debt — and it can seem like a godsend. But wait, how is ANOTHER debt supposed to help? Of course, you’re right to be suspicious. The thing is, it can help but only if you do it right. Do it wrong and you’ll be kicking yourself from a position worse than you’re in now. So, should I consolidate my debt? Debt consolidation can work as a way to pay off debt faster. However, if you’re not disciplined and look for help in the wrong places, you’ll end up spending MORE time paying off your debt. Let’s take a look at what debt consolidation is, how to consolidate debt, the pros and cons, where to find a reputable organization to help you, and ways you can get out of debt fast. What is debt consolidation?Debt consolidation combines all of the debt you owe into a single payment with a lower monthly interest rate. This typically works by taking out another loan in order to pay off all of your other debt. Let’s say you have debt across three credit cards and you owe the following:

Each month, you’re contributing $100 to each card for a total of $300 — however, a portion of each is being eaten by interest:

So in all you’re paying $254.16 towards your debt rather than the full $300. With debt consolidation, you take out a loan of $4,000 and pay off ALL of the above debt — and you get a lower interest rate for the loan at 10%. Now each month when you contribute $300 you’ll pay $266.67 towards your debt rather than just $254.16. In theory, this means you’ll be able to pay off your debt faster. The interest rate you’re able to get depends on which type of loan you attain:

If you want to get your debt consolidated, you’ll have to go through one of the two routes above — which we’ll get into later. Before we do that though, it’s important you know the dangers around consolidating your debt. The problem with debt consolidationBut before you click on one of those scammy internet ads marketing “DEBT CONSOLIDATION — BE DEBT FREE IN 3 HOURS,” consider the big drawbacks to debt consolidation: 1. It could take longer to pay down your debtIf there’s anything we’ve learned about human psychology over a decade of studying behavior and personal finances, it’s that things like that are easier said than done. For example, if the average person ends up saving $300 in interest payments because of debt consolidation, do you think they’ll use that extra money towards their debt OR do you think they’ll end up spending it? Most likely, the latter. Human willpower is limited. It’s the same reason why cutting out lattes or skipping lunch to save money doesn’t work. A person with 300 “extra dollars” might end up just blowing it on something else. What happens then is it takes longer to pay down debt. This results in even MORE fees they have to pay. Aside from diminishing willpower, many debt consolidation loan companies offer up longer loan terms than people realize. So while the interest rate is lower, they end up paying more because they didn’t take into account how long they’d have the loan for. 2. You could lose your home or carIf you decide to put your car or home down as collateral you stand to lose much more than a few thousand dollars off the life of your loan. A home equity loan is also known as a second mortgage. Taking a second mortgage out on your home means you risk losing your house if you fail to make payments. Of course there are some advantages to going this route. For one you can deduct the interest payments from your home equity loan from your taxes. Plus you’ll be able to get a lower interest rate than if you went the unsecured route. Overall, though, it’s just not worth the risk — especially when there are better ways to go about it. 3. Your credit score will sufferThere are a few things that go into making a great credit score. One of them is your credit history — or how long you’ve had credit for. It actually accounts for 15% of your overall score. That might seem small but consider this: If you get rid of a bunch of different lines of credit at once, your credit score is going to take a huge drop. That drop gets bigger with more and more lines of credit you close. How do you know if debt consolidation is right for you?Debt consolidation can be a great way to plan your route out of debt. But that doesn’t mean it’s the perfect solution for everyone. The benefits of debt consolidation are hard to argue with. You can simplify your debt, save money on interest, only deal with one creditor, and (hopefully) clear your debt faster. But there are pros and cons you need to know about before you make this decision. It can be the best move for some, but worse for others. Signs debt consolidation is right for youYou have high-interest debtsThe number one sign that debt consolidation is a good option for you is if you have several high-interest debts. Why pay interest on several debts when you can pay it on just one? If you know you can secure a lower interest loan, it makes sense to consolidate your debts. According to Experian, the average personal loan interest rate is 9.41% -- whereas the average interest rate for credit cards is around 16%. So, if you’ve got a ton of credit card debt, it’s worth considering debt consolidation. You have good creditIf you’re already in debt, getting another loan might be tricky unless you have good credit. Most creditors will want a credit score of around 670 (FICO Score). If you have good credit, you’re more likely to get approved, and also get a loan with decent interest rates. Remember, you want a loan with lower interest rates than your current debts, so this part is key. If your credit score isn’t the best, a new loan might not have favorable interest rates. You want a fixed repayment scheduleWith some debts like credit cards, it’s easy to just make the minimum payments or even miss a payment (please don’t do this). This makes it harder to clear the debt because some of it relies on willpower. With a personal loan, you have a fixed payment and loan term that you have to abide by. This makes it much easier to stay on track and clear your debts. It also means there are no fluctuations in your monthly debt payments like with a credit card so it’s easier to budget for. Signs debt consolidation is NOT right for youYou have a poor credit scoreHaving a poor credit score is one reason why a lot of people want to get out of debt as fast as possible. However, debt consolidation relies on you not only being able to take out a new loan but also getting one without crazy high interest rates. If the only loans you can take out mean you’ll be paying MORE in interest rates, then it’s not worth it. In this case, the only benefit would be to simplify your loans. But what you really need is to save on interest so you can clear the debts faster. You’re on the verge of bankruptcyIf things have taken a downward turn and creditors are threatening to sue, then a debt consolidation loan may not even be accessible to you. Bankruptcy is a scary thought, but if this is your reality, you are unlikely to qualify for a debt consolidation loan. If this is your current situation, you would be better off looking into debt settlement to try and reduce your debt amount first. You can’t afford the monthly repaymentsTaking on another debt is tricky if you’re already in debt. While you can use this one to clear your other debts, you need to make sure you can cover the monthly repayments. As it’ll be a higher debt amount (to cover all your other debts), the monthly repayments will be higher. Make sure that you can fit it comfortably into your budget before taking on new debt. After all, missing repayments can set you back even further. How to consolidate debt — and get rid of it completelyIf you’re STILL interested in consolidating your debt, I want to help you. Because there are a LOT of scammy consolidation services out there. These “businesses” will promise that they’ll help you get out of debt fast through their loan packages … … only to screw you with hidden fees, bloated interest rates, and long loan terms. The trick here then is to separate the good debt consolidation organizations from the bad ones. Step 1: Find a non-profit debt consolidation firmNon-profit debt consolidation firms are 501(c)(3) organizations that help provide you with consolidation services, credit counseling, and will even negotiate with your creditors for you. The best part: They do so with little to no costs to you since they’re funded by third-party sources such as donations and grants. Unfortunately, even scammers and bad consolidation services have non-profit status. So you’ll have to do your research into finding a reputable one. Two good signs a non-profit debt consolidation firm is the real deal:

Make a list of 5 to 10 non-profit debt consolidation firms. Spend the next week calling each of them and getting a consultation on your situation and what they can do for you. A good non-profit will spend about an hour on your consultation. Beware of any organization that wants to take your money and put you into a plan right away. They are NOT looking out for your best interests. Step 2: Eliminate temptationLuckily, a non-profit debt consolidation firm will take care of a lot of legwork for you. That means they’ll call your creditors, negotiate down your debt and interest rate, and work with them to consolidate all of your debt into one manageable monthly payment. Unluckily, that’s the easy part. The hard part means actually doing the work of paying down your debt — and that’s up to you. To do that, you need to first get rid of the temptation of using your credit cards until you’re debt-free. If you ever expect to pay down your debt, you can’t add more to it. Here’s my favorite tip: Plunge your cards into a bowl of water and shove it all into your freezer. Seriously. Remember what we said about human willpower? It’s very weak — so weak that a solution like freezing your cards is necessary sometimes to delete temptation. When you literally freeze your credit, you’ll have to chip away at a massive block of ice in order to get it back — giving you time to think about whether or not you want to go through with whatever purchase you were going to make. You can also give them away to a loved one to keep until you’re out of debt. Step 3: Confront your debtIt’s good to finally confront your debt. That’s the first step to getting out of it. While it may be tough to climb out of debt, the sooner you make a plan to do so, the better. You’ll be able to repair your credit score, work on boosting your savings, save on interest, and finally get some sleep at night. Debt can weigh heavily on the mind, after all. The good thing is, you don’t have to do this all alone. There’s help at hand. You can get in touch with a non-profit debt consolidation firm to help you. Take advantage of their credit counseling services to help steer you through unmanageable debt. Do your research and find a non-profit so you can avoid the scammers out there. It’s easy to feel bad for yourself and avoid confronting your debt. It’s harder to actually step up and do something about it. Since you’re here, that means that you’re willing to put in the work to dig yourself out of your financial hole which is amazing! What is the difference between debt consolidation and debt settlement?Another term you’ll likely come across in your quest to clear your debt is debt settlement. But what is it? Both debt settlement and debt consolidation are used to handle personal debt, but they work in very different ways. Debt settlement is used to reduce the total amount of debt owed. Whereas debt consolidation is about reducing the number of creditors you owe. With debt consolidation, you combine multiple debts into one. Debt settlement is when you ask one or more of your creditors to accept less than you owe. If the creditor agrees, you both reach a settlement agreement in either a lump sum or installments. Which one is best for you?This depends on your circumstances and what the creditor will agree to. If you want to make your monthly repayments more manageable and reduce the amount of interest you pay, then debt consolidation is the way to go. If you’re already behind on payments and are struggling to meet them, then debt settlement might be a better option. In this case, if you’re already behind on payments you might struggle to get a debt consolidation loan anyway because of the impact on your credit score. So, debt settlement is definitely something to try out to reduce the burden. Debt settlement is the next logical step if you’re out of options, have poor credit, and want to avoid declaring bankruptcy if at all possible. It may mean taking a hit on your credit score, but you might have to just accept that. Once the debts are clear, you can get to work on repairing that damage. How does debt settlement work?Debt settlement is a tricky one and requires you to whip out your negotiation skills. There’s no guarantee the creditor will agree, but there’s no harm in asking. The process is pretty simple. You can ask your creditor if they would be willing to negotiate a settlement. Do this over the phone or in writing to keep a record of the conversation. A creditor can do one of three things:

With the counteroffer, you will need to consider if the amount they want is affordable in your budget. Make sure you’re agreeing to something that’s realistic and fair. Once you agree on a settlement amount, all that’s left is to arrange the payments. This can either be a lump sum or through installment payments, whichever you agree to. After you’ve made the payments, the remaining balance that’s been hanging over your head will be a nice round zero. If negotiating debt settlement on your own sounds like a nightmare, don’t worry. There is help at hand. You can hire a debt settlement company to negotiate on your behalf. However, this does involve paying them a fee, and again, you have to do your research to avoid hiring a scammer. Pros and cons of debt settlementProsYou reduce your debt amountThe biggest pro to debt settlement is simply that you reduce your debt amount. A lot of people don’t know that you can ask your creditors for this. So they carry on struggling. But if you’re struggling, it can’t hurt to ask. If a creditor agrees, you could cut hundreds of dollars from your debt and all the interest that comes on top of that. You can clear your debt fasterWith a smaller debt amount to pay off, you can pay it off faster. Whether you agree on a payment plan or a lump sum, you’ll be able to say goodbye to your debts much sooner. This means your money will be freed up faster to put into savings accounts or whatever else you want to spend your money on. You can also get to work repairing any damage to your credit score once the debt is clearer. The sooner the better. It could help you avoid bankruptcyIf bankruptcy is on the horizon, debt settlement should absolutely be a consideration. The last thing you want is a bankruptcy on your record. You can pretty much say goodbye to being able to take out credit for a LONG time if you reach this point. ConsYour credit score will take a hitNaturally, debt settlement does not reflect well on your ability to repay debts. If you have debt settlement in your credit history, it signals to future creditors that you are riskier to lend to. This could result in sky-high interest rates or outright credit rejection in the future. However, if your credit score is already low and your debts are just making it worse, then you pretty much have nothing to lose. Yes, you’ll take a hit, but you’ll also get out of debt sooner if your creditors agree to debt settlement. You might struggle to get credit again… especially with those creditorsA lower-than-ideal credit score does affect your ability to take out credit in the future. However, if you’ve been in a tricky situation with credit, it’s probably worth avoiding new loans and finance for a little while anyway. The creditors who agree to debt settlement will likely avoid lending to you again because they will be worried about losing money. This could limit your options in the future. But if it’s your only option, you might just have to just bite the bullet. There is no guarantee creditors will agreeUnfortunately, if you’re relying on creditors to throw you a lifeline here, you might be out of luck. In an ideal scenario, they’ll be forgiving and offer you a way to climb out of debt in a way that benefits everyone. But there’s no guarantee they’ll do this. They could outright reject your request or be inflexible with their counteroffer. There’s little you can do if this is the case. You can try another of your creditors if you have several debts to see if any of them will agree. Avoiding debt in the futureAfter you’ve decided on a method to reduce your debt – don’t stop. Ridding yourself of debt is just one key part of building strong personal finance. The other part of the puzzle is to manage your spending so you don’t end up in the same position as before. The last thing you want to do is put all your hard work into clearing the debt, only to succumb to temptation or poor money management which puts you right back where you started. That’s why we want to give you something that can help you take your personal finances to the next level: The Ultimate Guide to Personal Finance. In it, you’ll learn how to:

Enter your info below and get on your way to living a Rich Life today. 100% privacy. No games, no B.S., no spam. When you sign up, we’ll keep you posted Debt consolidation: How does it work and is it right for you? is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/debt-consolidation-how-does-it-work-and.html September 27, 2021 at 08:34AM

Is Renting a Waste of Money? Ramit Sethi Explains

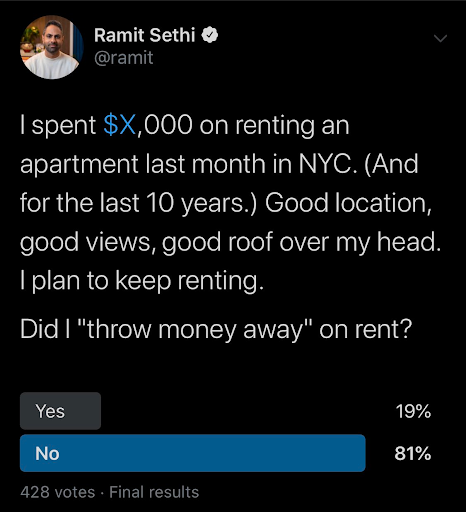

I know, I know. You’ve been told you’re “throwing money away on rent.” Someone in your life made you feel guilty for not buying a house and building equity. And let me guess: They said something like, “Ugh, I just hated paying someone else’s rent!” Right? There’s just one problem: It’s not true. First, let me ask you a simple question: Do you “throw money away” when you eat out at a restaurant? Of course not. You’re paying for value. Yet somehow this logic totally falls apart when you apply it to real estate. I decided to run a poll on Twitter to ask what people thought.

Not surprisingly, 95% of people said, “No, you didn’t ‘throw money away’ on a nice meal.” Then I asked the same question — but for rent.

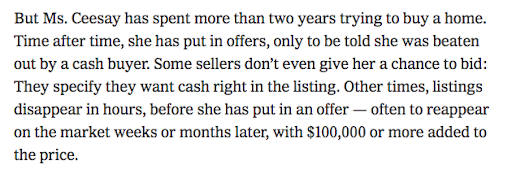

LOL! Notice the drop from 95% to 81% when I asked if I was ‘throwing money away renting.’” In other words, many more people believe that renting is throwing money away. You and I know that if we spend $20 eating out, we were happy to spend it to get good food, table service, and someone who cleans up our dishes. Paying for rent is exactly the same: You’re paying for a roof over your head (the meal). You’re also paying for a landlord to deal with any paperwork and maintenance issues (the service). So why do so many of us blindly repeat this phrase that we’re “throwing money away on rent?” Why do people believe that rent is a waste of money?Understanding why this myth persists is the first step in understanding the truth about buying vs renting. Check out these reasons why many people believe that rent is a waste — what do you notice? 1. PropagandaThe powerful real estate lobby, the government, and our parents all tell us that “real estate is the best investment of all.” There are even governmental tax incentives to buy! Repeat this for decades and a population starts to blindly believe, rather than running the numbers. Here’s a tiny glimpse of how the real estate propaganda machine works. In this article from the New York Times, buying a house subtly portrayed as the ultimate, foolproof way to get rich in America. Fast. Hurry! Prices only go up! Add in HGTV, economic malaise, & phrases like “you’re throwing money away on rent.”

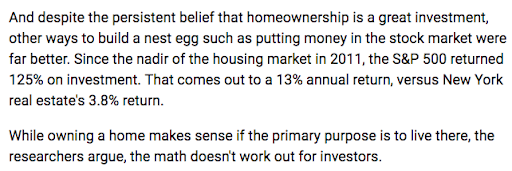

“Minus expenses.” LOL. Given that “expenses” can run over 10% of a house’s selling price, that’s like me saying, “I really enjoyed this trip to the Grand Canyon! All except for the part where my son fell off a cliff and died. Anyway, it was fun!”

In reality, real estate is not always the best investment. It comes with significant phantom expenses. And there are often better investments, such as a simple low-cost index fund. This is well-understood by sophisticated investors but ordinary Americans have been duped into thinking their primary residence is a great investment. Often, it is not. (I could buy today but I rent by choice because it is a better option for me.)

Bonus: Want to learn a better way to master your finances and build real wealth? Download my FREE Ultimate Guide to Personal Finance.

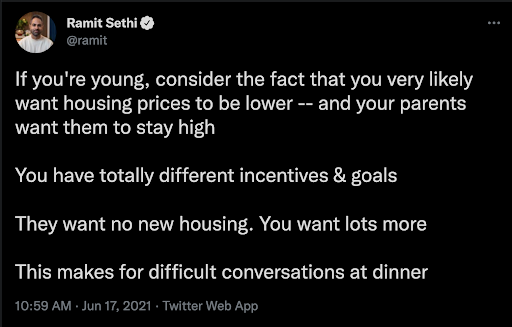

2. Financialization of real estateIn America, we believe that our house should also be an investment. Why? It’s not like that in many other countries. In fact, if you sit down at the dinner table with your parents, they want the price of their house to stay high — while younger people want the price of housing to go down!

3. The idea that someone’s “getting one over on you”Americans HATE the idea that someone is making money off them. A Reddit comment said (paraphrased) “If you buy, it might cost more but at least you won’t be paying your landlord’s rent.” Do you understand how crazy this is? When you eat out, do you say, “I like the food here but I just hate paying this restaurateur’s rent?” Of course not. We only repeat this phrase with real estate. Stop it. 4. Lack of understanding about phantom costsPeople believe if you buy a house for $200K and sell it for $450K, you made $250K. This is false. They don’t understand maintenance, taxes, and other phantom costs, and they don’t compare ROI to other investments. Also, did you know real estate prices also go down? 5. Following the same playbook as alwaysBuying a house was, in general, a good thing for most Boomers. There were also fewer low-cost investment options like index funds in the 70s and 80s. Therefore, stuck in the past, they parrot the same lessons to millennials, who face unaffordable housing, stagnating wages, and better investment options. This is the problem when people (Boomers) recommend something, but don’t actually understand why it works: They just keep repeating it, over and over, even though the situation has changed.

Bonus: When it comes to your finances, you shouldn’t be following the same old playbook. Download my FREE Ultimate Guide to Making Money to learn a better way.

What you should know about buying vs rentingRenting isn’t necessarily better than buying and buying isn’t necessarily better than renting. It depends on many things:

My advice: Run the numbers and get educated. But never, ever say you’re “throwing money away on rent.” Is Renting a Waste of Money? Ramit Sethi Explains is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/is-renting-waste-of-money-ramit-sethi.html September 22, 2021 at 08:34AM

How to nail any phone interview (the ESSENTIAL 2021 guide)

Looking to nail a phone interview you have coming up? Well read on. Interviewing is hard. One of the few ways to make it even harder is to make it a phone interview. In-person, you can read and respond to all of the interviewer’s physical cues, but on the phone you’re often left to guess if they’re engaged in what you have to say or busy checking their inbox while you ramble on. Unfortunately, many application processes begin with a phone interview. I used to hate phone interviews…at least until I learned a few simple tips that turned this typically uncomfortable conversation into a job offer — or a follow-up, face-to-face interview — every time.

What is the purpose of a phone interview?In a phone interview, the interviewer wants a condensed version of your story and why you’ll be good for the job. It’s your foot in the door and a critical part of the interviewing process. It acts as a screening interview to narrow down the candidates. How to prepare for a phone interviewYou may think it’s simply making sure your phone is loud enough to hear it over reruns of Friends as you contemplate changing out of your pajamas into fresh pajamas. But if you really want that job, you’ll want to take it as seriously as any in-person interview. These are our top phone interview tips. 1. Prepare for what you needIf you’re a compulsive list-maker, eat your heart out because this is your time to shine, baby! List everything that you’ll need during your interview slot:

Bonus: Want to finally start getting paid what you’re worth? We show you exactly how in our Ultimate Guide to Getting a Raise and Boosting Your Salary

2. Prepare yourselfBusiness at the top and party at the bottom might help save face during video interviews, but it does nothing for your confidence. Shower, do your hair, do makeup (if that’s you), and get dressed as if you’re going for the in-person interview. At the very least, get out of those pjs and wear some grown-up shoes. Who knows, this might switch over to a video screen interview without warning. 3. Prepare your responsesKnowing what to say during the actual interview will rely a lot on your level of preparedness. Recruiters often post some questions along with the job offer, and those questions give you insight into the topics up for discussion during the interview.

Bonus: Want to work from home, control your schedule, and make more money? Download our FREE Ultimate Guide to Working from Home.

4. Know what you want from the interviewBefore you answer that interview phone call, make notes on your expectations of the role and the company.

These are just a few examples of possible questions. It’s important that you know what you want from your new role and whether it’s worth the change from the existing one. Practicing for your phone interviewYou didn’t think you were going to get out of this without practicing, didya? Practicing allows you to plan out the interview and make adjustments as you go along. So here’s what you do. You’re going to phone a friendPrep your friend with an interview question list and press “GO!” If possible, record the conversation so you can listen to the exchange afterward. You’ll be surprised how many strange quirks you might have, for instance, constantly clearing your throat or saying “um” all the time. Use the mirrorThis may seem like a bizarre tip, but hey, trust us. When you practice your scripts in the mirror, you immediately start making subtle changes such as changing your posture, fixing your hair, and possibly even smiling. These are all little efforts to boost your confidence and shouldn’t be taken lightly. Just do it! Make notesWhether you’re practicing with a friend or your reflection, takes notes of things you observe and your responses to the questions. Before your telephone interview, be sure to go through these notes again just to keep them top of mind. Pump yourself upInstead of thinking about the interview as scary and something you would rather not do, psych yourself up. Start telling yourself that this is going to be a fun interview, even if you need to be professional and alert. Do what it takes to get yourself motivated as the excitement and energy will carry through to the interview. Practice small talkIf you’re a straight-to-the-point kind of person, this might be a tough one to swallow. Small talk might seem superfluous and juvenile, but it’s a necessary means to an end. It allows you to build rapport with the interviewer and it also gives you that legroom to relax before bombarding the other party with stories of your greatness.

Bonus: Want to know how to make as much money as you want and live life on your terms? Download our FREE Ultimate Guide to Making Money

During the interviewThis is your moment in the ring and while it might just be the first knockout round of the tournament, show up for it in a big way. Be professionalEven if you’re applying for a job as a children’s entertainment manager on a cruise ship, any job you apply for will have some form of responsibility, so professionalism is still important. You can talk about the elements of fun, but try to remain on topic and answer the questions as thoroughly yet concisely as possible. Don’t rambleIt’s tempting to start pulling out all those stories from your story toolbox and just run with it, but chances are good that you’ll miss the question and end up boring the interviewer. Respond to the question and keep it short yet informative. StandIt’s a natural instinct to want to hunker down and protect your vitals, but it doesn’t translate well over the interview. By standing up, you improve the blood flow which is a quick energy boost. This allows you to literally think on your feet as those questions start coming in. Standing also boosts confidence, by the way, and who doesn’t need an extra boost? Watch your breathingBreathe. Focus on measured breathing but make sure it doesn’t sound like you’ve just run a marathon on the other side. Steady breathing also does wonders for circulation, which is needed when you’re cornered with the OG of questions, “So tell me about yourself.” When you’re breathing is erratic, the body tries to protect the organs which could leave you feeling dizzy and disorientated. Which seems normal for an interview, right? But trust us, you don’t have to have a racing heart and sweaty palms. Be promptYou want to start off strong and this means that you need to be prepped and ready. Be ready for that call and don’t let it ring more than three times. You want the recruiter to know you were ready and waiting for their call. Use a greeting that is professional and a little more than just “Hello.” A rule of thumb is to start off with your name, “Hello, this is Joe Greene.” Anything more than this might just be a bit much before the other person has had a chance to introduce themselves. When they do, let them know that you’ve been expecting their call and that you’re excited about the interview. SmileYep, we’re back with this one, but only because it’s so dang important. Something changes in your vocal cords when you’re smiling. Plus, there’s that positive effect smiling has on your nerves, to consider. You’ve practiced this in the mirror, so now it’s just a matter of applying it during the interview. Trust us, it’s pretty hard to sound happy and upbeat when you’re not smiling. Be the voiceThere are few things that put people to sleep faster than a one-tone drone. Make sure to add some excitement to your voice by alternating the pitch slightly. While that monotone voice might be your usual style, it comes off as lacking interest. Ouch! While you’re at it, check your volume. You want to be heard, but you also don’t want to blast the interviewer’s eardrums. The final voice trick is to make sure that the pace is good. While there is too slow, slow is still better than too fast. The last thing you want is losing the interviewer because they can’t keep up with your runaway soliloquy. Acing a phone interview depends a great deal on keeping the other party engaged throughout the call. Prepare yourself for potential issuesThe neighbor suddenly starts their renovation project in the middle of the interview, or there’s a medical emergency, or your phone battery decides to retire, whether you’re on charge or not. Decide beforehand how you will handle events like these and have a plan B. For starters, you might want to have a second phone handy or another place to conduct the interview, that’s easily accessible within a few seconds. Or, worst case, you might have to phone the interviewer back as soon as you can and apologize. Ask whether it’s possible to reschedule. The Bottom LineKnowing how to do well in a phone interview relies a lot on your ability to stay calm and focused. Preparation will get you halfway there, and the other half is just harnessing your inner best self through little confidence boosts along the way. Success comes with following sound advice, applying what you learn, and preparing for all eventualities. If you want to learn more about landing your dream job, we’ve got you covered!

Do you know your earning potential?Take my earning potential quiz and get a custom report based on your unique strengths, and discover how to start making extra money — in as little as an hour. How to nail any phone interview (the ESSENTIAL 2021 guide) is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/how-to-nail-any-phone-interview.html September 17, 2021 at 04:34PM

What Is Strategic Asset Allocation? Definition + Allocation Strategies

Strategic asset allocation is the practice of setting a goal for each of your asset classes (e.g., stocks, bonds, cash), and rebalancing it every year as you realize earnings on your investments. This is a great tactic if you want to:

In this post, we’ll walk you through how to set up your asset allocation in a way that makes sense for your goals.

What are investment assets?When you invest, your money goes into different assets. These are government bonds, mutual funds, stocks, retirement savings, and even real estate. Not all of these assets carry the same risk. For instance, stocks are deemed riskier than say government bonds. Choosing your ideal mix of assets will depend on various factors including:

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Why do we recommend strategic asset allocation?Strategic allocation allows you to be intentional about your investment choices, without being chained to the mundane of everyday management. Sure, you might have to spend some time on it, but make it a once-a-year thing if you can. So how do you do this? Automated investments. You can automate everything from the money that goes from your bank account into the fund, to choosing funds and assets. You can even put a mandate in place for fund switches when there’s a serious market nosedive. How to set up strategic asset allocationFirst, let’s start with an example: Imagine you’re a 24-year-old who just opened up a brokerage account with $3,000. If you want to employ strategic asset allocation, you’ll want to set certain percentages you’ll want in each asset class based on your goals. Since you’re young and have many years before retirement, you might be more willing to take risks with your portfolio. Considering this, you decide to be aggressive and put your money in 80% stocks ($2,400) and 20% bonds ($600). A year later, you discover that your stocks accrued 20% from your initial investment, while your bonds have earned you just 2%. This leaves your assets at 82% stocks ($2,880) and 18% bonds ($612). Now your assets are “unbalanced” in accordance with the goals you set for them and it’s time to rebalance them. In order to stay in line with your strategic asset allocation strategy, you’ll need to take 2% or about $57.60 out of your stocks and into your bonds. That’ll leave your portfolio nice and balanced at 80% stock and 20% bonds once more. Of course, your goals will change over time. As you get older, you’ll find that you might want to be more conservative with your investments, and you can change your asset allocation percentage so they fit your needs. Consider the following scenarios, including your timeline and risk tolerance to help you figure out the best asset allocation strategy for you. Determine your investment timelineYour asset allocation should be adjusted according to the amount of time you have to invest. For instance, if you have a one-year goal or a fifteen-year goal, the investment strategies should look different. The shorter the term, the less risk you should have in your portfolio. Ideally, investments should run for a minimum of ten years to get the most out of the markets. Assess your risk toleranceRisk tolerance is how much risk you want to expose your capital to. An aggressive approach might not be for everyone, even if they have 20 years plus to ride out the markets. It’s important that you are comfortable with your risk tolerance because there is always an opportunity for loss in investing. The higher the risk, the higher the chance of loss. But there’s also a chance of higher earnings. The point is, you need to be comfortable with the potential of your risk class compared to the potential for total loss. Determine your goalsWhat is the point of investing and how will strategic asset allocation play into those goals? If your goals are to spend as little time micro-managing your investments as possible, then strategic allocation is your best investment friend. Add to that investment automation and you’ll have plenty of free time to do whatever you want instead of scouring newspapers, widgets, and indicators for hours a week trying to maximize your returns. Sure, there is a time to intervene but knowing when and how often is what will allow you to strike a good balance.

Purchase funds in each asset classThis is a simple way to make sure you have a nice, diverse investment portfolio. And diversity matters. Remember when financial pundits were telling everyone that property was the safest portfolio and that the likelihood of a market crash was just, well silly? Turns out that did happen and well, we literally refer to it as the mortgage crash. Now, property is still worth looking at when considering your investment strategy because the market did quite a rebound. But here’s the thing. Don’t tie all your money up in that one asset that seems to be going well at that point in time. Those who were able to wait it out managed to make their money back and then some. Those who retired at the time of the crash, not so much. Split your assets as much as possible to increase your chances of good returns and reduce your risk. Even when you’re investing in an asset, for instance, stocks, split those funds even more. Consider index funds that include a basket of funds so you’re as diverse as you can possibly get.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Rebalance your portfolio every 12-18 monthsIn order to stay balanced, you’ll need to check out your portfolio and rearrange funds in order to stay in accordance with the allocation percentages you set as a goal. Strategic asset allocation vs tactical asset allocationNow, it’s worth mentioning that these asset allocation strategies don’t exist in isolation. Also, strategic asset allocation is just one method of dealing with your investments. There’s also no rule that says if you choose one method, you need to stick to it for the next thirty or forty years. It’s not unusual for you to use several methods at times, even if you have a main method. For instance, you can opt for strategic allocation, and at times, employ tactical allocation. Tactical allocation simply means you’re in the thick of it all the time, making even the minutest decision regarding your investments. It’s the opposite of the hands-off strategic allocation model. Fund managers often use a tactical approach to asset allocation and it works, because they know what they’re doing. The goal here is to maximize profits and when this is done, the portfolio is returned back to its original state. It’s only supposed to be a temporary measure. There are other allocation methods too.

To concludeInvesting can be as easy or as hard as you want it to be but when your portfolio strategy is all about asset allocation, you’re one step closer to a healthy asset mix. But if you really want to know all the ins and outs of investing, saving, and more, you should check out our Ultimate Guide to Personal Finance. Enter your info below and get on your way to living a Rich Life today. 100% privacy. No games, no B.S., no spam. When you sign up, we’ll keep you posted What Is Strategic Asset Allocation? Definition + Allocation Strategies is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/what-is-strategic-asset-allocation.html September 17, 2021 at 01:34PM

How to Choose a Career that You’ll Love (even if you don’t know what you want to do)

How do most people choose a career? Well…they don’t. They stumble into a job after college, take whatever they can get, then follow one of the few paths available from that random job. No wonder most people are frustrated in their careers. But there actually IS a way to narrow down your potential interests to choose a career that you will love. Ramit Sethi, our founder and career-path guru, has put together a Dream Job system that helps you explore ALL the careers you’re interested in, test each to see if you’d really enjoy doing them, and move on to other jobs if they’re not a good fit. Here are some of our best tips on finding a career you love – even if you have no idea what you want to do.

1. Understand yourself and your personalityA good evaluation of your personality defines the kind of job you would fit into. And we’re not talking about taking a random career personality test and doing whatever it tells you to do – those tests are usually unrealistic, and can’t paint a clear picture of what really drives you. Instead, ask yourself the following questions and let your responses guide your career search.

Bonus: Want to fire your boss and start your dream business? Download our FREE Ultimate Guide to Business.

What motivates you?The first step in assessing your personality is finding out what motivates you. If you can’t answer that question on your own, turn to friends, family, and colleagues to understand your driving force. When do they recognize your eyes lighting up? Maybe it’s after you’ve helped someone, or when you’ve solved a difficult problem. Understanding what gives you energy can help point you in the right career direction. Evaluate your skillsSome jobs tap into soft skills, like communication and personality, while others demand a particular academic skill set. For instance, technical jobs automatically require you to possess an analytical mindset/background. You cannot apply for a scientific research position when your only training is in art history. If you do want to make a career switch, that’s ok, but understand that you’ll likely need additional training. Understand your weaknesses and dislikesHave some self-awareness and get clear on your major weaknesses and dislikes. You may realize that you have poor delegation skills or that you hate team collaboration. You’ll need to recognize where you have weaknesses or outright dislikes. For example, if you don’t like talking to people, you probably won’t want to consider a career in customer service. 2. Make a list of potential careers to exploreOne of the most daunting parts of choosing a career is picking just ONE job…that you’re supposed to do for the rest of your life.

Just start by listing ALL the careers and job titles you might be interested in. Anything you want to explore, just write it down.

Ramit call this the Cloud Technique because your options are as open as the sky. This lets you say “Yes” to EVERYTHING you’re curious about instead of constantly saying “No, I can’t do that because…” Where should your ideas come from? Here are a few career brainstorming tips:

Bonus: Want to finally start getting paid what you’re worth? We show you exactly how in our Ultimate Guide to Getting a Raise and Boosting Your Salary

3. Research your top choicesOnce you’ve tentatively selected a few job titles, it’s time to do some deep research. This is where you go from “Hmm…sounds interesting” to truly understanding what the job is about. Remember: You don’t have to become 100% knowledgeable about these roles… just yet. You just want to learn as much as you need to see if a job is right for you. Let’s use the job title of “engineer” as an example of what you’ll want to look for. The first thing, you’ll want to do is get a bird’s eye view of the job:

You can find this info with a quick search through Wikipedia or Googling “introduction to [INSERT JOB].” As you tackle those broad and sweeping questions, you may start to eliminate some options you originally listed. And that’s okay. In fact, that’s expected. Just because something sounds interesting in theory, doesn’t always mean it will be. You actually want to narrow things down in this stage. If at any point, you run out of job titles on your list, simply go back to step three (with your new insights on what you want from a job) and start again. Once you have a basic high-level understanding of the positions, you can dive deeper into the nitty-gritty details:

Bonus: Want to work from home, control your schedule, and make more money? Download our FREE Ultimate Guide to Working from Home.

The whole time you’re going through this process, ask yourself “Could I see myself doing this?” and “Is this something that still interests me?” This process helps you discover what it is you truly enjoy. Once you’ve narrowed your list down again, you’re ready to hear from people who actually work in these roles. That’s how you guarantee this is the right career choice. 4. Conduct informational interviewsAn informational interview is an informal talk you have with a subject working in your desired profession. It is the last step you take when deciding your career path. You may have heard about informational interviews before, but few people actually take this critical step. Two things you need to know:

Here’s how to set up an informational interview: Book their timeFirst, identify people who you’d like to speak to. Then, reach out with a friendly email asking if they’d be willing to meet with you. Here’s a sample email script you can modify and use. Subject: Hello, Allen! I hope all is well and that this email finds you in good spirits. I’m thinking of catching up on a few things regarding my career choice. I read about quality control in large pharmaceutical companies and am passionate about it, but there is not much information on the ground experience. The job will have me on the production line, and I’m interested to know what that looks like and what should I be ready for? I know you are resourceful, given your over a decade-long career in the same line, which I admire greatly! Would you mind virtually connecting with me for a brief period where I can get your ideas on quality control as a line engineer? Please let me know a good time to connect. Kind Regards, Tommy Keep it short. Go straight to the point and give a compelling reason. Prepare talking pointsYou don’t want to show up to an informational interview with nothing to say. Prepare your questions ahead of time, and do a little research on the person you’ll be interviewing, too. This will help you connect with them while getting the most out of the interview. Speak about your challenges truthfullyAn informational interview is the perfect place for you to share reservations about the job you’re learning about. After all, you haven’t chosen it as a career yet. It’s better to find out that it’s not a good fit for you now than in the future once you’ve started in that line of work. Be a good listenerBe attentive and take notes during your informational interview. Ask questions during the conversation. If you don’t know what to ask, you can always ask an open-ended question like, “Is there more you can tell me more about XYZ?” Send a thank-you noteSending a thank-you note is mission critical after an informational interview. Even if you don’t want to go into that line of work after the interview, you never want to burn a professional bridge by not following up. Drop the person you spoke with an email and let them know how their advice is helping you achieve your goals. While a dream job falling into your lap is rare, you can systematically find one. We see many students struggle to get a job of their choice, and we step in to help. This is not to say that it is always easy. But it is possible. Let us help set you up for success by guiding you on a career path you love. Let us help you in your quest to find your dream job.

Bonus: If you’re worried about your personal finances, you can improve them without even leaving your couch. Check out my Ultimate Guide to Personal Finance for tips you can implement TODAY.

Do you know your earning potential?Take my earning potential quiz and get a custom report based on your unique strengths, and discover how to start making extra money — in as little as an hour. How to Choose a Career that You’ll Love (even if you don’t know what you want to do) is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/how-to-choose-career-that-youll-love.html September 15, 2021 at 04:34PM

Should I Buy a House Now?

Buying a house has been sold as a major part of the American Dream, but for many people, it doesn’t make sense for financial or lifestyle reasons. There are some good reasons to buy a house, but it’s important to examine your reasons before you make one of the biggest financial decisions of your life. Here are 5 guidelines to help you decide if you’re ready to buy a house.

Will you live there for 10+ years?When you buy a house, a long time horizon matters because of the enormous fees involved in buying and selling a house. There are closing costs, taxes, furniture, realtor costs, and maintenance. Closing costs for selling a house run around 10% of the house’s selling price. This means that if you sell your house for $300,000, closing could cost you $36,000 or more. And that’s just closing costs! If you move in a short period of time — for example, four years — those fees will dwarf any equity gains you may have. Imagine driving a car off the lot: We all know that it instantly loses value. The same is true of your house, and it takes time to amortize (or spread) the costs over a long period of time. Most people stay in their house for less than 8 years — and that number is actually higher than it’s been in several decades! Before the 2008 financial crisis, the average length of time that Americans stayed put was only around 4 years. Don’t give in to the peer pressure to buy a house if you might not stay there for the long term. If you know that you want to move in fewer than 10 years, you will likely make more money by renting and investing in S&P index funds.

Bonus: If you’re looking to buy a house, it’s important to ditch debt, save money, and build real wealth. Download my FREE Ultimate Guide to Personal Finance to learn how.

Is your total monthly housing cost lower than 28% of your gross monthly income?Your total housing costs should be less than 28% of your gross income. When housing costs exceed 28%, you run the risk of being overwhelmed with expenses if something goes wrong (e.g., an unexpected repair, job loss, etc). Use the 28/36 Rule to see if you can afford your housing. Here’s an example:

Why gross income? I use gross because it’s easy to calculate. Everyone knows their gross income and taxes complicate net income (different people choose different deductions). However, if you prefer to use net income, go for it! I love hearing when people create their own point of view on their finances. Exceptions to the 28/36 rule

Have you saved a 20% down payment?If you haven’t saved a 20% down payment, you’re not ready to buy a house. Why? Not just because of PMI, which is an additional fee you’ll often pay when you get a mortgage without 20% down. The real reason to save 20% before buying is counterintuitive: Building the habit of saving is critical before you buy and have unexpected housing expenses such as a broken water heater, roof, or unexpected taxes. I frequently get frustrated comments about how “impractical” this rule is. “How am I supposed to save 20%? That will take years!” Yes, it will. Which is exactly why you should save now. Saving is a habit, which is better practiced before your mortgage is at risk. If you write a comment like this, you are not ready to buy a house Note: I don’t mean that you have to put 20% down. In some cases, such as low interest rates, many people intentionally choose to put a small amount down. But you should be able to.

Bonus: Having more than one stream of income can help you reach your savings goals faster. Learn how to start earning money on the side with my FREE Ultimate Guide to Making Money

Are you OK if the value of your house goes down?If you are buying because you believe the price of a house always goes up, reconsider: Real estate is not always the best investment. Here are some good reasons to buy a house

Notice what’s not on the list: “You need the price of the house to go up.” Maybe it will — if so, great! Maybe, once you factor in expenses and opportunity cost, you could have gotten a much better return in a simple S&P index fund. Buy for the right reasons.

Bonus: Are you thinking about buying a house with more room to work from home? Make sure you find your WFH dream job first! Download our FREE Ultimate Guide to Working from Home.

Are you excited about buying?If you’re approaching buying a house with dread — like a heavy feeling of obligation or peer pressure — just stop. You don’t need to buy and you should never feel guilty for renting. I rent by choice. If you’re truly excited about buying, then you might be ready to buy. Final thoughts on these rulesYou don’t need to follow any of these rules. Your money is yours. In fact, I’m sure you can point to someone who bought a house with 3% down and did fine. But you’ll rarely hear from people who made disastrous housing decisions. They simply disappear, never to admit their mistakes. Many times, they don’t even know why they got into trouble. I hear from hundreds of them every month. And I can tell you that these rules will keep you out of the biggest sources of financial trouble for people who buy a house. These are conservative rules that will keep you out of trouble. Yes, they might take you more time to buy. And yes, you might see people seemingly “skip the line” and buy a house before you. But for the biggest purchase of your life, I believe you should be conservative. Take your time — there’s no rush. Most of the time, when you hear people in a big rush to buy, it’s not a careful consideration of facts — it’s fear that they’ll be “priced out” or an emotional rush from seeing headlines of houses selling for way more than they can afford. Many people who end up in financial trouble skip these rules. Don’t be one of them.

Do you know your earning potential?Take my earning potential quiz and get a custom report based on your unique strengths, and discover how to start making extra money — in as little as an hour. Should I Buy a House Now? is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/should-i-buy-house-now.html September 15, 2021 at 09:34AM

Best Performing Stocks of The Past 12 Months

This market is tricky and when you’re looking to make money from it, it becomes important to analyze all the best-performing stocks and compare your portfolio to the current S&P 500 to make an informed decision.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.