|

All About Stocks and Bonds: What You Need to Know

Investing is the single most crucial thing you can do to ensure your financial future — and the sooner you start, the easier it is to get rich. There is more than 100 years of evidence in the stock market that suggests this. Stocks and bonds are a great place to start, so we’re going to dig into that in this post. But first, let’s talk about the typical perceptions of investing.

People still don’t understand what investing is exactly. Folks seem to think there is some magical way to make a fortune with stocks and bonds. From what I’ve seen, the two things people get most wrong about investing are thinking:

And, frankly, you have every reason to believe this. Thanks to Hollywood and the (annoying) talking heads on cable news, we’ve come to think of investment as a maniacal creature that’s not suited for the average person… and many of us just don’t understand exactly how investing works. That’s why we want to dispel some of those myths and notions surrounding investing by focusing on some of the most common topics you’ll hear when it comes to investments: How do stocks and bonds work? How can you balance them in your portfolio? What’s the difference between stocks and bonds? This article isn’t going to be about which stocks are hot right now or what sort of investment strategy is going to make you into a zillionaire today. If you’re looking for something like that, I suggest you go back to watching the pundits on cable news. SPOILER ALERT: Cramer has done much worse than the S&P 500 since 2008. Instead, stick around for a no-BS lesson all about stocks and bonds, what they are and what part they can play in your investment future. How do stocks work?When you own a company’s stock, you own part of that company. Stocks are also called equity for that reason — you own a tiny piece of the company.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Stock basicsIf the company does well, your stock will do well. So, ideally, you want to invest in strong-performing companies. You can buy and sell whenever you want through your broker or self-serve sites like E*Trade or TD Ameritrade. Inevitably, whenever I’m teaching someone about the basics of stocks, someone will pipe up with a myriad of questions like these:

First thing’s first: SLOW DOWN. Before you make an investment in any sort of stock, you’re going to want to stop and ensure you understand how to go about deciding what stocks to buy. Understanding stocks is the first step before you start piling your money on whatever looks good on the day. Choosing the right stockThe simplest way to narrow down the universe of stock options is to think of companies you like and use. Take some time right now to write down 15 companies you use and return to time after time. Think of everything. For example:

Instead of 5,000 stock options to choose from, you now have 15 companies you could possibly invest in. Remember: A good company isn’t necessarily a good stock! For any stock, you’re going to need a deeper analysis than “I think khakis from Gap are awesome, so I’ll buy stock from them!” Instead, you’re going to want to look at 5 different areas:

You can get all of this information online for free — and you’d be wise to do as much research as you possibly can. If you see a reason to doubt a company based on any of the areas above, avoid that stock. Bonus: Want to know how to make as much money as you want and live life on your terms? Download my FREE Ultimate Guide to Making Money Stock research resourcesHere are some great websites to help you start out:

At first, all of the charts, earnings, and balance sheets will be incredibly confusing — but the more you look into them the more you’ll start to get a good sense of what’s going on. It just takes practice. Advantages of investing in stocks

Disadvantages of investing in stocks

Bonus: Want to know how to make as much money as you want and live life on your terms? Download our FREE Ultimate Guide to Making Money

What are bonds?Bonds are like IOUs that you get from banks. You are lending them money in exchange for a fixed amount of interest. Bond basicsIf you buy a 1-year bond, the bank says, “Hey, if you lend me $100, we’ll give you $102 back in a year.” The approximate current rate of return for a 2-year bond is about 2%. (Check here for the up-to-the-second number.) Overall, bonds are:

With these qualities, what kind of person would invest in bonds? Well, anyone who wants to know exactly how much they’re getting next month should invest in bonds. It doesn’t matter if you’re in your twenties or if you’re in your seventies. If you want a stable investment — despite the lower returns — then bonds are for you. After all, some people just don’t want the kind of volatility the stock market offers. And that’s fine. Advantages of bonds

Disadvantages of bonds

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

What’s the difference between stocks and bonds?Now we’ve covered the basics of what stocks and bonds are, let’s take a closer look at the main differences between them. The main ways stocks and bonds differ are in three ways:

Type of returnThe first way that stocks and bonds differ is in how the owner gets a return on their investment. With stocks, because you own a piece of a company, you can receive dividends. These are company profits handed out to shareholders. With bonds, you receive a return through interest gained, because what you’ve bought is basically a debt. Another way to make money with either stocks or bonds is to sell them for a higher price than you bought them, but this depends on a lot of different factors. Return guaranteeThe one thing that pretty much everyone knows about the stock market is that it’s risky. There are zero guarantees that you will make your money back, never mind more on top of that. That’s the main thing that puts people off from investing in the stock market. Those who are especially risk-averse might have a happier time with bonds though. As bonds are debt investments, the company or government you buy the bond from has to pay you back. There’s no way around it, so this is good news for you. You get a guaranteed return on your investment in the form of interest. The downside is that the returns are usually much lower than stocks. BenefitsThe third way stocks and bonds differ is with benefits. The good thing about stocks is that you’re a shareholder, which means you could have voting rights within that company. This does depend on the shareholder setup, however. So, don’t expect to waltz through the doors at Apple HQ and make big changes because you bought one share. With bonds, on the other hand, the main benefit you can get is preferential treatment when that bond matures. What is equity vs. debt?The two types of investment you need to know about are the equity and debt markets. These refer to two different ways investments are bought and sold. In the debt market aka the bond market, investments in loans are bought and sold. In the equity market or stock market, it’s equity in a company that’s bought and sold. Generally, the equity market is deemed a higher risk than the debt market. How does the bond market work?The bond market or debt market works by a company taking a loan out. Instead of heading over to the bank, they’ll get that funding from investors who buy bonds. The company then pays an “interest coupon” which is the annual interest rate paid on a bond. Bonds fall into either short-term, medium-term, and long-term. Short-term bonds “mature” or are paid off essentially within one to three years. Medium-term bonds last around ten years and long-term bonds mature over much longer periods of time. Do you earn capital gains on bonds?Capital gains are what you earn after you sell an asset for more than you bought it for. For example, if you purchase a house and it shoots up in value by the time you sell it, you just made a capital gain. In the stock market, if you sell a stock for a higher price than you bought it, congratulations, you just made a capital gain. But what about bonds? Bonds are a little trickier because they’re typically a bit harder to sell than stocks. With bonds, your source of income is related to interest rather than equity income. Bonds are often not held until they hit maturity and are sold before then. If you do this, you might earn a capital gain (or loss) depending on what has happened to the company that sold you the bond. If you manage to sell your bond for higher than you bought it, this is a capital gain. How does the stock market work?The stock market or equity market is a market where the share of ownership in a company is bought and sold. There are two main ways to make money from stocks--dividends and selling. Owners of stocks can profit from dividends, a percentage of company profits that shareholders receive. It might be a bit weird to think of yourself as a shareholder… but that’s exactly what you are if you own a stock. Depending on a myriad of factors, whoever owns stock can also profit when they sell it. But this only works if the market price has increased since you bought it. The stock market is a bit more volatile than bonds. Stocks can shoot up in value or plummet for a whole range of reasons. Stocks can be affected by social changes, politics, economic events, or even the CEO tweeting (eye roll emoji). This makes them a riskier investment, but that’s why you need to educate yourself on them. And if you’re still here congratulations! How should you balance stocks and bonds in your portfolio?So now we’ve covered the basics of stocks and bonds, the question is: What do you invest in? You can do either stocks or bonds but a mix of the two is a popular choice. It spreads your risk and diversifies your portfolio--something you should always aim for. But which should you invest more in? The safer, guaranteed but low returns of bonds or the higher risk, higher reward stocks? Well, there’s no clear-cut answer here. It all depends on…

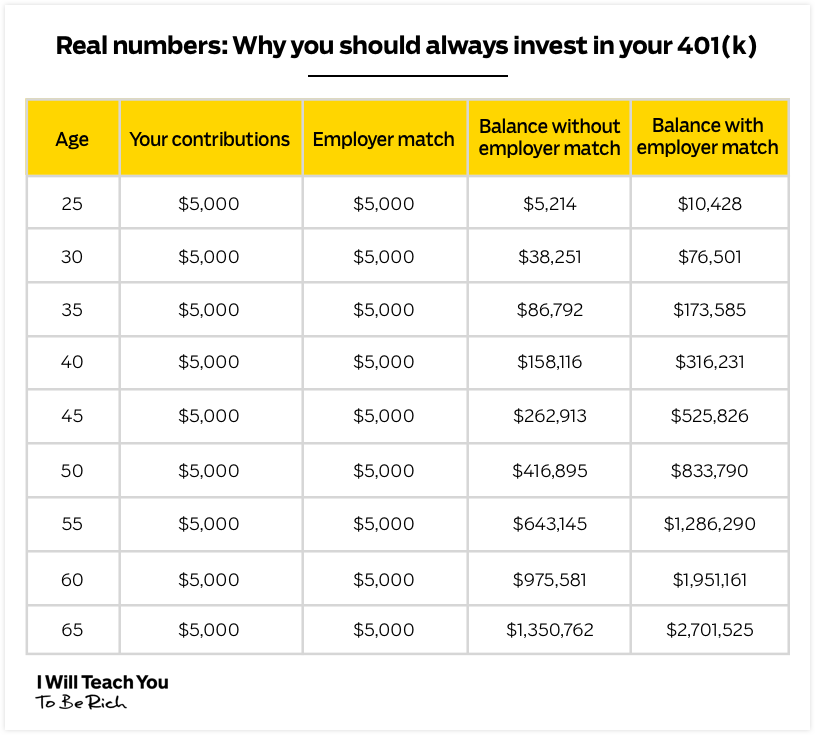

Investment portfolios all fall somewhere on a scale of super aggressive to conservative. A super aggressive investment strategy would be to put 100% of your money into stocks. A conservative portfolio would have no more than 50% in stocks. For moderate growth, you’ll want to look at more of a 60/40 split of stocks and bonds. How does that relate to retirement? If your portfolio is a key part of your retirement strategy, then the amount of risk you should take depends on how close you are to retirement. In other words, if you’re nearing retirement, you don’t want to dump all your money on high-risk stocks. You’ll want to rebalance your portfolio to be a bit safer and predictable. In this case, you’d probably opt for the more conservative split. Those who are younger have a bit more flexibility because generally, the more time in the market, the more time your portfolio has to recover if it takes a dip.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

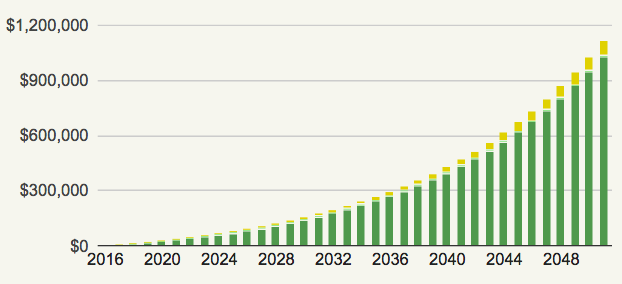

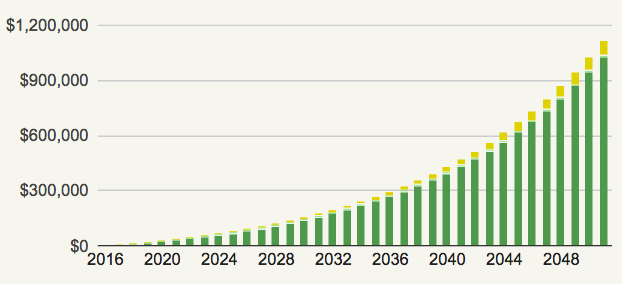

How do you start investing in stocks or bonds?So now you’re all filled in on what stocks and bonds are, how do you start investing in them? As the taste for investing grows, so do the options available to us. Now it’s easier and more accessible than ever. Here are a few popular options to get started: Use an online brokeragePossibly the most popular method of investing is to use an online brokerage. This works much in the same way as a traditional in-person broker does but the fees are lower and you can do it all through your smartphone. Online brokerages let you buy all types of investments including individual stocks, funds, and bonds through a website or app. Mutual fundsAnother popular way to invest is to use a mutual fund instead of investing in individual stocks. Mutual funds are made up of several different companies so the risk of investment is spread rather than targeted and risky. Unlike many online brokerages, mutual funds typically have a dedicated fund manager who picks the best investments for you. This means they come with much higher fees as a result. Index fundsIndex funds are made up of a group of companies so the risk is spread. The main difference between index and mutual funds is that index funds are passively managed. This means they’re the cheaper option and they’re also the less volatile option. Rather than trying to beat the market, index funds watch it and make sensible investments. Robo-advisorsIt might sound a bit sci-fi, but it’s pretty simple. A robo-advisor is a digital platform that invests your money through automation and algorithms. There’s little or no human contact involved (great for introverts) so it’s a very hands-off type of investing. Investment managersFinally, if you have the cash to splash and want to make some serious investments, hiring a dedicated investment manager is another option. This is the most expensive option as you’ll be getting advice and tailored service. So it’s not ideal for those who want to save money on fees. IWT’s investment philosophyWhen it comes to what you want to invest in, stocks and bonds are both solid investments — as long as you do your research. What I think EVERYBODY should be doing when it comes to their investments is simple: low-cost, diversified index funds. Let’s look at a real-world example. Say you’re 25 years old and you decide to invest $500/month in a low-cost, diversified index fund. If you do that until you’re 60, how much money do you think you’d have? Take a look: [insert graph from original article] $1,116,612.89. That’s right. You’d be a millionaire after only investing a few thousand dollars per year. Smart investments are about consistency more than chasing hot stocks or anything else: The two essential ways to invest your money are straightforward:

Note: If $500/month sounds like a lot, read all the ways you can free up that money with just a few phone calls. If you are just starting out, it’s so awesome that you’re here. For financial security, it’s more important than anything else to start early. And don’t worry if you think you’re a little late to the game. After all, the best time to plant a tree was 20 years ago…the second-best time is NOW. Man, I’m starting to sound like a fortune cookie. Get started on your personal finance journeyIf you’re looking into investment, congratulations! You’re making an important step in securing your financial future. Investment isn’t the only thing to think about though. Nor are stocks and bonds. For a full-picture approach to personal finance, be sure to check out The Ultimate Guide to Personal Finance. In it, you’ll learn not only how to understand stocks and bonds, but also how to:

Bonus: Want more advice on how to improve your finances? Sign up today and get your free copy of The Ultimate Guide to Personal Finance.

Do you know your earning potential?Take my earning potential quiz and get a custom report based on your unique strengths, and discover how to start making extra money — in as little as an hour. All About Stocks and Bonds: What You Need to Know is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/all-about-stocks-and-bonds-what-you.html September 03, 2021 at 02:34PM

0 Comments

How To Dispute Credit Card Charges The Easy Way (just 3 steps)

Getting charged for something we didn’t pay for sucks. As Ramit, our founder and ultimate money man points out, your credit card can either be one of the coolest parts of your personal finances or the absolute worst. One of the best things about using a credit card is your ability to dispute charges. This is because credit card companies want to keep you as a customer, and they will do whatever they can to keep you charging. Let’s have a closer look at disputing credit card charges and what rights you have as a consumer.

What does it mean to dispute a credit card charge?Disputing a credit card charge means that you want to question a charge on your bill. Let’s face it: We’re online more and more, which also means that we’re most likely shopping more, which means we’re using our credit cards more than we ever thought. These charges can quickly add up, and it’s never a bad idea to consider the ammunition we have in the event we need to question a charge that just doesn’t look right. When we knowingly buy a certain product or service, we may skip the Terms of Services — and unknowingly agree to certain stipulations (think early termination fees, the requirement to give 60 days notice to cancel, and the like). The more we become accustomed to shopping and buying online, the stronger we think we get. But, here and there, companies get sneaky — and you have tools to fight back when needed. What types of charges can you dispute?There are generally three types of charges that you can dispute on a credit card: 1. Fraudulent chargesYou would obviously want to dispute this immediately (go right to Step #3 below under Exact Scripts: How to dispute your credit card charge). The faster you act, the sooner you will avoid even bigger credit issues. For example, if the fraudster maxed out your credit card, you will be blocked from making additional purchases using that card. Further, your higher credit usage or what they call “credit utilization” might be reported to the credit bureaus, affecting your credit score. (Yes, another potential dispute you might need to make.) Remember that credit card companies take fraud very seriously. When you call to report the fraudulent charge, they will most likely cancel your card immediately and send you a new one with a different number. This might sound extreme, and for sure, it’s inconvenient, especially if you have recurring charges set up with a particular merchant, or if you use the credit card for daily purchases. 2. Billing errorsBilling errors come in all shapes and sizes. Here are some examples of billing errors that you might be able to dispute on your credit card:

When you begin the dispute process for a billing error, make sure to double or even triple-check why the amount is in error. There could have been a discrepancy in price or an extra fee that the merchant did not make you aware of. Taxes are always confusing, too. They might not be calculated when we check out, but suddenly appear later after the transaction has been completed. After having undergone various billing disputes, buying online always gets our worst instincts going. Make sure that tiny checkboxes are unticked for, “Yes, please subscribe me for monthly shipments of [Product X]!”

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

3. Quality of goods and servicesThis one’s a bit tougher to dispute because it does not fall under the regular Fair Credit Billing Act dispute process. Generally, if you were charged for something that you just don’t feel right paying for, you can dispute the credit card charge based on quality. This could mean a product or service for which you are aware that the purchase was made but it is simply not up to par or not delivering for you what it is supposed to deliver. Obviously, if you ordered a pair of shoes online and they arrived but in the wrong size or wrong color, you wouldn’t just call up your credit card company to dispute the transaction. You’d want to call up the merchant first to try and get the right shoes sent to you. But what about a monthly subscription for a class that just isn’t doing it for you? You did what you could to cancel, but they’re just being jerks about it, telling you that they’re sorry, but there simply isn’t anything they can do for you? This is where disputing the charge with your credit card company comes in handy. This type of credit card dispute requires a little bit more work, but Ramit has you covered. You will need to go through with all three steps below in order to get the charge removed from your account. What types of charges can you not dispute?We all have buyer’s remorse: after leaving the store, you regret buying that 55″ Smart TV. Or maybe you bought the 55″ Smart TV at Best Buy, then later realized you could have gotten it cheaper at Walmart. Either way, you cannot get a refund by disputing this charge on your credit card. Instead, you would need to return the item to the merchant and adhere to that merchant’s particular policies and procedures. In fact, before you dispute a charge — whether a strange-looking merchant name or a strange amount you see on your credit card statement — do a bit of homework first. It’s quite possible that you did knowingly make a purchase for an item or service at an agreed-upon amount, but it renders differently on your statement. Sometimes a Google search of the unrecognizable merchant name will reveal the true name of the company. Then, you’ll have that facepalm moment, “OH YES! Now I remember.” You can also do a search of your email inbox, as oftentimes a copy of a receipt is emailed to you as a way to double-check the charge. You might also want to check with the other folks who you’ve authorized to use your credit card to see whether they’ve made any recent purchases that you’re not aware of. It’s never a bad idea to do a little bit of homework first on a particular charge before disputing it with the merchant or the credit card company. How long do you have to dispute a charge on your credit card?According to the Fair Credit Billing Act, you must send your letter within 60 days of receiving the first bill showing the error you wish to dispute was mailed to you. Ramit suggests doing it sooner — which isn’t impossible, since most credit card companies these days allow you to view your account balances and activity either online or via the mobile apps of their issuing banks. While some credit card companies allow you to submit a claim online or via email, it’s never a bad idea to still send your dispute letter by snail mail. To be double sure, send it by certified mail with a return receipt, so you have even more proof that your letter was sent and received. The creditor must acknowledge your complaint in writing within 30 days of receiving your dispute letter — unless, of course, the problem has already been resolved within that time frame. The creditor has two billing cycles — but not more than 90 days — to investigate your claim and resolve the issue. When the investigation is complete, the credit card company must send you the results in writing. If the company confirms your dispute and agrees that the charge was in error, the amount must be credited back to you, known as a chargeback, along with any related finance charges. However, if the credit card company concluded that the charge was indeed accurate, you are on the hook for paying the disputed amount, along with any accrued finance charges during the investigation period. Don’t agree with this decision? You can appeal. You have 10 days from receiving the explanation to write to the creditor and let them know that you’re not going to pay. Of course, if you choose not to pay, the creditor has the right to start collection proceedings. And that’s when things could get ugly. You don’t want things to get ugly. These credit billing laws have been in place since the early 1970s to protect consumers and are curiously relevant even today. People should get their money back if they feel that they have been charged incorrectly. To put credit, billing, and disputes in perspective, are there any Bitcoin or cryptocurrency aficionados reading this? Well, for all of the hype surrounding the blockchain and decentralized finance, there is one downside to paying for goods and services with Bitcoin: there are no chargebacks. That means that ALL SALES ARE FINAL. If you buy with Bitcoin and want your money back, you are SOL, as they say. This is probably one reason why there are no credit cards denominated in cryptocurrency. (We here at IWT are not making judgment calls about investing in Bitcoin or cryptocurrency, but keep this in mind when using it as a method of payment.)

Bonus: Want to know how to make as much money as you want and live life on your terms? Download our FREE Ultimate Guide to Making Money

Exact scripts: how to dispute your credit card chargeStep 1: Dispute the charge at the sourceRamit advises that this step is optional because you can get your money back without having to interact with the merchant. However, in the spirit of providing all options possible, you can get your money back from the source. In many cases, such as billing or math/calculation errors, merchants do want to do the right thing because they do want repeat business — and they want you to leave them 5-star reviews online. Further, you might have a relationship with the merchant and you don’t want to ruin it due to an error on their part. Here’s an email script Ramit suggests that you can use to begin the process of disputing a charge: SUBJ: Erroneous charge on statement Greetings, I went over my credit card statement today and discovered that I have been charged an extra month for my gym membership. Could you refund my money back as soon as possible? If not, I plan on disputing this charge with my credit card company. I look forward to this situation being fixed promptly. Best, Ramit Notice something about this email? it’s simple and to the point, but it leverages your credit card company as an ever-so-slight threat. Businesses HATE fighting credit card companies in disputes. So you’ll often be able to get your money back based on that alone. To help consumers with this process, the Federal Trade Commission provides a handy sample email you can use to file a complaint with your merchant. However, no matter which letter you choose, Ramit suggests you include the threat of disputing with your credit card company into the message. After you’ve sent the email, expect the merchant to get back to you soon. You might be thinking: What merchant WOULDN’T respond to a dispute like this? You’d be surprised. Smaller Amazon or eBay sellers might not get back to in a week (or at all), as they have a small staff (they literally are Mom and Pop), or are located in far-flung locations over the globe. For digital subscriptions, the staff might be even smaller: one person, responsible for creating the course, selling it, and handling customer service. Sometimes messages get lost. If they haven’t contacted you and given you a full refund within a week of sending the email, move on to the next step. It’s not worth waiting for them if they’re going to treat you like that. Step 2: Gather all relevant information to dispute the credit card chargeAside from your credit card company, your most powerful ally in the fight against the merchant is you and information. So before you even think of calling your credit card company, gather any and all information you might have that is related to the charge you want to dispute. This includes things like:

If you want to take your game to the next level, create a recordkeeping system that can be your best weapon against businesses trying to take advantage of you. After all, things can get really heated when you’re disputing charges. Instead of getting mad, open a spreadsheet that details the last time you called, whom you spoke with, and what was resolved. Here’s a great template you can work from. Call date Time Name of rep Rep’s ID #Comments You can download the tracker here. You wouldn’t believe how powerful it is to refer back to the last time you called, citing a rep’s name, date, and call notes. You can even ask for an email address to which you would happily send this spreadsheet displaying your history of doing business with this merchant. Most businesses will fold like a lawn chair if they know you’re not here to mess around. This information is going to be vital in the next step of the process. Step 3: Contact your credit card companyAfter you’ve completed steps 1 and 2 above, now it’s time to get down to brass tacks and call your credit card company. To make things convenient for IWT readers, we’ve provided a list of phone numbers from the major credit card issuers you can use to dispute the charge:

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Most of these companies will send you to an automated voice menu when you call. There you’ll have the option to dispute a charge. (Note: if it’s fraud, you’ll be immediately transferred to a separate department, and during that call, your credit card will be canceled and you will be issued a new card.) You’ll then be put into contact with a representative. Simply tell them, “I want to dispute a charge on my credit card statement,” and describe the situation using the information you’ve gathered in step two. Your credit card company will then open an investigation into the matter and issue you a temporary credit until their case is resolved. Once they’ve (hopefully) found that you were in the right, they’ll issue something called a chargeback that will refund you the credit and charge the merchant what you originally paid. If you want to email your credit card company, here’s a great script you can use to contact them straight from the Federal Trade Commission. Dear Sir or Madam: I am writing to dispute a billing error in the amount of [ $______] on my account. The amount is inaccurate because [describe the problem]. I am requesting that the error be corrected, that any finance and other charges related to the disputed amount be credited as well, and that I receive an accurate statement. Enclosed are copies of [use this sentence to describe any information you are enclosing, like sales slips or payment records] supporting my position. Please investigate this matter and correct the billing error as soon as possible. Sincerely, [Your name] REMEMBER: You need to do this within 60 days of the charge appearing on your bill. Once they receive the complaint, they’re legally required to respond to you within 30 days. The process will be roughly the same as when you talk to them on the phone — they’ll open up an investigation, issue you temporary credit, and either facilitate a chargeback or deny your complaint. No matter what happens… congratulations! You now know how to dispute your credit card charges. Final WordsLove ’em, hate ’em, credit cards are here to stay. Understanding how credit cards work, building and maintaining good credit, and how you can make them work for you — such as disputing charges — will help you live your Rich Life. 100% privacy. No games, no B.S., no spam. When you sign up, we’ll keep you posted How To Dispute Credit Card Charges The Easy Way (just 3 steps) is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/09/how-to-dispute-credit-card-charges-easy.html September 03, 2021 at 02:34PM

3 common buyer’s remorse purchases (and how to avoid them)

So you spent a small pile of money on something you THOUGHT you wanted — only to realize later you could have gone without it. Congrats! You have buyer’s remorse. It’s not fun BUT there are ways to prevent it. We’ll show you how. |

RSS Feed

RSS Feed