|

How Much Should You Really Have in Your 401k (by age)

At IWT, we talk about 401ks – a lot. (See here, here, or here for proof) And, that’s with good reason. If you want to be rich, the 401k is one of the most powerful investment tools at your disposal, especially for retirement planning. It is also one of the most misunderstood money-maximizing vehicles, starting with how much you should have in your 401k. That is a solid question, but it doesn’t have a simple answer. To answer that burning question -- How much should I have in my 401k? -- we need more details. How much to invest in 401k investments will depend on your age and a few other considerations. Let’s start at the beginning.

Bonus:If the COVID-19 pandemic has you worried about money, check out my free guide on Coronavirus-Proofing your Finances with the CEO approach

What is a 401k?A 401k is a powerful type of retirement account that many companies offer to their employees as a perk. With each pay period, you put a portion of your paycheck into the account. It happens automatically so you don’t have to do anything special and there are a ton of benefits. A 401k is called a “retirement” account because it gives you huge tax advantages if you don’t touch your money until you reach the minimum retirement age of 59 1/2 years. While you will have to pay a penalty if you touch your 401k savings before you reach retirement age, the benefits far outweigh the risk. Here is a snapshot of the benefits of having a 401k: Tax benefitsThe money you contribute to a 401k isn’t taxed until you withdraw it, which you can’t do without penalty until you reach 59 ½. This means you have much more money to invest for compound growth. In comparison, if that money was invested in a normal investment account instead, a portion of it goes towards income tax. Also, you have some control over how much you withdraw. With careful planning (definitely talk to your accountant for this one) you can minimize your tax burden (win-win) Employer matchMost companies offering a 401k will match you up to a certain percentage of your paycheck. In many cases, they will match their employee contributions 1:1. To put that in perspective, let’s say your company offers 5% matching. Now, if you earn $100,000/year and invest 5% of your annual salary ($5,000), your company would match you $5,000 — That doubles your investment without costing you a cent. It’s free money! Not basically free, “like” free, or practically free. It is FREE MONEY and you are leaving it on the table if you don’t take advantage of the employer match. Plus, if you don’t invest in a 401k with employee matching, you are missing out on all the returns that free money will generate. It adds up.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Automated contributionWith a 401k, your money is taken from your paycheck and invested automatically, which means you don’t have to go into a brokerage account to invest each month. You don’t actually have to do anything. Your 401k contribution is deducted from your paycheck the same way that your federal income tax or health insurance premium is deducted. This is an excellent psychological trick to keep you investing. Check out the graph below that illustrates why you should always invest in your 401k:

So, one good answer to “How much I should have in my 401k?” is at least enough to get the employer match. And really, there are only two reasons for you NOT to invest in a 401k: 1. You’re trapped on a desert island, and the employee benefits are lacking. 2. Your current employer doesn’t offer a 401k. What is the maximum 401k contribution amount?Starting in 2020 (and for tax year 2021), you can contribute up to $19,500 each year to your 401k if you are under 50. If you are over the age of 50, you may be able to make catch-up contributions. This provision lets you invest up to an additional $6,500 in your 401k (tax years 2020 and 2021). PRO TIP: You need to be behind in your 401k contributions to make catchup contributions. When compared to a Roth IRA, where you can only contribute up to $6,000/year, this is an amazing opportunity — especially since your pre-tax money is being compounded over time. How much should you have in your 401k by age?Now that we have established that you need a 401k in your life and explained how much you can contribute, let’s talk cash. Aside from investing enough to meet your employer match, how much should you have in your 401k, really? One way to answer that question is to look at your age. While there is no one-size-fits-all answer to the question, “How much should I have in my 401k?” there are some best practices you can keep in mind to guide your efforts. Yes, while you should start investing in a 401k as soon as possible, some people might not get that opportunity right away — and that’s okay. The point is to do it when you can. When you do finally start investing, there are a few good rules of thumb to help you make a sound decision on how much you should have in your 401k. Age 30Ideally, you should have at least one year’s worth of income in your 401k. That means if you make $60,000, you should have at least that much saved in your 401k. Age 40Once you hit 40, you should have at least three years’ worth of income in your 401k. That means if you were making $80,000 by the time you turned 40, you should have at least $240,000 saved in your 401k. Age 50When you turn 50, you should have at least five years’ worth of income in your 401k. This means if you increased your income to $100,000, you should have $500,000 saved up in your 401k. By retirement (age 65)Once you reach 65, you should have at least eight years’ worth of income in your 401k. That means if you increased your income to $150,000, you should have $1,200,000 saved up in your 401k. Is your 401k savings on track?Have you met your mark? If you aren’t there yet, don’t panic. These are just rules of thumb. That means they only give you a rough estimate of what you should ideally have by the time you hit these ages. They do not take into account your individual income and experiences -- or other investments you might have in play. In reality, there’s no one hard answer to how much you should have in your 401k — and anyone who tells you otherwise is either lying to you or just doesn’t know much about finance. We could pull up a bunch of figures and show you how much someone in their 20s or 30s is saving — but that would be a complete waste of time for two reasons: 1. It’s impossible to compare two investors fairly. Everyone has their own unique savings situation. That’s why it’d just be dumb to compare the Ph.D. student saddled with thousands in student loan debt with the trust fund baby who just snagged a cushy six-figure corporate gig the first month out of college. They’re both going to save very differently, so it’s not worth comparing. 2. Most people aren’t financially prepared for retirement. The American Institute of CPAs recently released a study that found that nearly half of all Americans aren’t sure if they’ll be able to afford retirement. That’s even scarier when you consider the fact that many people underestimate how much they’ll need for a comfortable retirement. So instead of worrying about minutiae like how much you “should have” saved, focus on the future. What’s important is that you: • Do your research. You are already doing that by reading this article, but don’t stop here. Keep reading. We recommend Investing for Beginners and How Much Do I Need to Retire? • Be disciplined. This means consistently putting away money and not touching it (except in rare situations -- more on that here). Do not treat your 401k as a savings account or an optional expense. Make regular contributions. • Start early. The best time to get started investing was yesterday. The second best time is right now. Wherever you are in your financial journey, get started as soon as possible. Investments earn returns, but those returns can compound over time. That’s why it’s so important you understand exactly what your 401k is — and why it’s so important to your retirement strategy. So, how much should you invest in your 401k?Okay. So, while investing is highly personal and financial goals should be personalized, you are here so we can teach you to be rich. We have some advice to get you started. How much you should actually be investing each month depends on a system we call the Ladder of Personal Finance. Check out this video, or read about the Ladder below: 1. Your employer’s 401k match. Each month you should be contributing as much as you need to in order to get the most out of your company’s 401k match. That means if your company offers a 5% match, you should be contributing AT LEAST 5% of your monthly income to your 401k each month. We’ve already discussed the importance of this – don’t throw away free money and the returns from that free money. 2. Whether you’re in debt. Once you’ve committed yourself to contributing at least the employer match for your 401k, you need to make sure you don’t have any debt. Remember, if you have employee matching, you are effectively earning a 100% return on every penny you invest in your 401k -- that is significantly more than the interest you would save by paying down your debt. If you don’t, great! If you do, that’s okay. You can check out my system on eliminating debt fast to help you. 3. Your Roth IRA contribution. Once you’ve started contributing to your 401k and eliminated your debt, you can start investing in a Roth IRA. Unlike your 401k, this investment account allows you to invest after-tax money and you collect no taxes on the earnings. As of writing this, you can contribute up to $6,000/year ($7,000 if you are 50 or older). Once you’ve contributed up to that $6,000 limit on your Roth IRA, go back to your 401k and start contributing beyond the match. Remember, you can contribute up to $19,500/year on your 401k if you’re under 50. So, you should have no issue continuing to invest in your 401k. And if you are able to max it out, please be sure to give us a call. We’re going out for drinks -- on you. “But, why would I max out my Roth IRA before my 401k if it’s so good?”There’s a lot of nerdy debate in the personal finance sphere about this very question, but our position is based on taxes and policy. Assuming your career goes well, you’ll be in a higher tax bracket when you retire, meaning that you’d have to pay more taxes with a 401k. Also, tax rates will likely increase in the future. The Ladder of Personal Finance is pretty handy when considering what to prioritize when it comes to your investments, but it is just a tool. For more about the Ladder of Personal Finance and how to make it work for you, check out THIS video where I explain it. PRO TIP: The video is less than three minutes long. It is worth your time. Start earning more for a better financial futureThe answer to “How much should I have in my 401k?” is an important one — but it’s not the only way to ensure your financial future. We are going to let you in on a little secret. It is one that has helped thousands of people live their Rich Life: There’s a limit to how much you can save, but there’s no limit to how much money you can earn.

Bonus: Want to know how to make as much money as you want and live life on your terms? Download our FREE Ultimate Guide to Making Money

Many people don’t understand this and because of that, they’re content with contributing very little to their retirement accounts. When they actually retire, they’re surprised when their nest egg is a lot smaller than they thought and they have to get a job as a Walmart greeter to pay for their condo. If you realize that your earning potential is LIMITLESS, you can truly get started working toward living a Rich Life today. We recommend three ways to start earning more money: 1. Negotiate a salary raise. 99% of people are content with not asking for a salary raise. So if you are willing to negotiate, that puts you in the 1% and showcases to your boss that you’re a Top Performer willing to work hard for more money. 2. Start a side hustle. One of my favorite money-making tactics is starting your own side hustle. We all have skills. Why not leverage those skills to start earning more money in your free time? 3. Practice conscious spending. If you want to be rich, you have to start spending money like a rich person. No, I don’t mean going out and buying a Corvette. I mean spending money consciously so you know exactly how much you have to spend each month — while earning money passively. We want to help you get started on one of these tactics today: Starting a side hustle. We know. We know. The word “side hustle” tends to dredge up images of people working odd jobs and late hours, running errands, or making something to sell — but the reality isn’t like that at all! Freelancing is one of the easiest ways to have a side hustle, and you can get started right now. Living a passive-income lifestyle with little to no work is a fantasy. If you are serious about earning additional income, you have to take an active role in your side hustle. Eventually, you may be able to earn money passively -- but why would you be content with that. More is more, and we can show you how to get there. That’s why we want to offer you my Ultimate Guide to Making Money. We created this all-inclusive guide because we were sick of the awful advice that we found masquerading as legitimate money-making tips. Stuff like: • “Earn $100k a year in 4 hours a day.” • “You can make money by joining an MLM opportunity.” • “You just need to learn to live within your means.” UGH. No. You cannot expect to earn that much money with only a few hours of work when you are just getting starting. If you can earn $100k per year in 4 hours a week, why would you only 4 hours a week? We want to maximize earns AND have a good quality of life. MLM opportunities and other ready-made side hustle solutions only make money for the people selling them. You can make more as a freelancer than you would from any of those pre-fab solutions. Living a good life can mean going outside of your budget. If you are working late hours at a side hustle, you may need to have a sandwich for dinner to get it all in before bedtime or you may opt to order takeaway from a restaurant instead of taking the time to cook. There is nothing wrong with that. Your Chinese delivery or sandwich ingredients cost maybe $10. If you are earning $400 on your side hustle and that convenience means you can work through the evening, it makes cents (see what we did there?) Enter your info below and get the PDF for free today — and start the extra money you need to make your retirement goals come true. 100% privacy. No games, no B.S., no spam. When you sign up, we’ll keep you posted How Much Should You Really Have in Your 401k (by age) is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/how-much-should-you-really-have-in-your.html October 28, 2021 at 10:34AM

0 Comments

Should I Pay Off My Student Loans Or Invest? Here’s How To Decide

Student loans in America average near the $40,000 mark, and it makes it difficult to decide whether to invest or pay off student loans. Because, let’s face it, getting out of debt and saving for retirement is equally as important. Pay down debt or invest? Factors to considerThere are three elements that determine which route will suit your needs best. These are:

But before you dive in, it’s important to understand external factors may affect your decision. Your personal financial positionA critical factor in deciding whether to pay down your debt as opposed to boosting your retirement savings is the effect the move will have on your finances. Things to consider, include:

Bonus: Making more money can help you get out of debt faster while still having room to invest. Learn how by downloading our FREE Ultimate Guide to Making Money

The amount of your debtThe average student loan debt of $40,000 might seem doable, especially if you’re earning a decent paycheck. But let’s consider those specialist degrees where your student loans creep up to the hundreds of thousands of dollars. Suddenly this amount seems like a behemoth and it might not make sense to throw money at anything else until you get this huge number under control. The flipside is that with all those years you devote to paying off your student loans, you could have built up your retirement savings. You may want to predetermine a goal that will give you some wiggle room to focus on investments. For instance, you might set the goal that once you reach the halfway mark of your debt, you’ll start contributing to your retirement accounts. Remaining yearsIf you’re right at the beginning of the loan period, for instance, fresh out of college and working that first job, your priorities might be different to someone close to retirement. The cost of your financeThere are only a few instances where the debt interest rates are lower than what you would earn on an investment, but it happens. When it does, you want to make sure that you’re getting the best value for money. A low-interest rate student loan might just be better off with that minimum installment if you haven’t maxed out your 401(k) just yet. However, if the interest you’re paying is on the higher end, you might want to consider paying your debt first before increasing your investment contributions. Student loan options – which one’s yours?Fast-tracking your student loan payments can save you a stack of money in the long term. For instance, an extra $100 goes a long way to clearing off the interest portion faster. Here’s an example. Let’s say you have a $10,000 student loan at a 6.8% interest rate with a 10-year repayment period. If you go with the standard monthly payment, you’ll pay around $115 a month. But look at how much you’ll save in interest if you just pay $100 more each month:

It’s worth knowing that there are a number of options open to those who wish to pay off their student loan debt. Understanding the type of loan that you have (or are planning to take on)There are three student loan types to consider: federal, private, and refinance loans. Each has its own set of rules and carries a few pros and cons. A big plus across the board, however, is the fact that you can pay extra or make prepayments into an education loan without penalty charges. How’s that for an incentive? Federal student loansThe government makes provision for loans for students in order to access higher education. Instead of students borrowing from banks and other financial institutions, these loans are entered into with the federal government. There are three types:

Positives include that it’s easier to apply for a federal loan and in times of hardship, there are deferral and forbearance options. They also tend to offer lower interest rates as the rates are controlled by the government. It’s important to note that these loans carry costs and charge an initiation fee of 1.057% to 1.059% for regular student loans and 4.228% to 4.236% for PLUS loans. Private student loansThere are a number of private student loan products offered by banks and other institutions. What’s great about these loans is that they can tailor the loan type to suit the need, for instance, there is a loan for bar exams, another for medical school, and even a product for those with bad credit. These loans tend to be a little more costly and while there aren’t initiation costs, the interest rate is not fixed by the government. This means that the rate can be substantially higher than that charged on federal loans. Applicants will also need to show a good credit score. It’s also worth knowing that these loans aren’t part of any government forgiveness programs. So why get it at all? Turns out these loans are great for those who have high study costs. Student loan refinanceHigh-interest rates on a student loan are a real kick in the teeth and what better way to get your own back than by opting for a product with a lower rate? Student loan refinance products are offered to students who have a decent credit score with the aim of reducing their interest rate. This is not a great option for those with federal loans, however, as you will lose the federal protections and benefits should you opt to refinance.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Your retirement optionsSaving for retirement is an essential component of building wealth. It also happens to have tax and other benefits that you simply can’t get from regular savings or investments. But how do you make the decision to pay your future self when you still have debt? It will be easier to unpack that mule of a question when you understand retirement investment options a little better. Roth and Traditional IRAThese retirement plans allow you to contribute to your retirement savings up to a certain threshold per year. In 2020 and 2021, this annual threshold was $6,000. That means that if you’re worried about paying off debt or saving towards retirement, first check that you’re not already maxed out on these contributions. It’s worth noting that a Roth IRA also has an earnings limit of $140,000 for individuals. 401(k)There is no cheaper way to fund your retirement than a matched 401(k). Read that again. If you have extra cash lying around and you’re not maxed out on this, you’re losing out. Let’s explain. A matched 401(k) means that your employer will match your 401(k) contributions either fully or partly up to a certain percentage. Now just bear in mind, there is a limit of just under $20,000 per year, or 100% of your salary, whichever is the smallest. How to pay down debt while investingKnow what your financial position isOkay, we’ll admit it, you’re going to have some work to do. But a little bit of effort now will save you a ton of financial admin in the future. There are a few things you need to know before you can make a decision about whether to pay student loans or invest.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Use the envelope systemAn envelope system is a budgeting tool that allows you to allocate all your money to payments, savings, and such. It works on the premise that, if you had cash, you would stick your dollar bills into various envelopes and then mail them off to cover the bills. An envelope system works well because you decide the categories. While housing and utilities are a given, you can also have an envelope for lattes, entertainment, etc. Sure, you can decide that the biggest chunk of your salary goes to Target, but the point is to cover your expenses and bills, put aside money for saving and investing, and still have some fun money. When you’ve used all your entertainment money, the idea is that it’s done. When the envelope is empty, that’s when you stop. Not only will this allow you to allocate more effectively, but it will also stop the frustrating overspending that seems to befall us when we’re low and there’s this great pair of shoes… stop! Now, here’s the great part. You can have an envelope for additional payments to your student loans AND you can have an envelope for investments. Choose investment options that suit your pocketWhen you have to ask the question, “Should I pay off my student loans or invest?” chances are good that you’re not interested in spending a ton of cash on fees and expensive investment products. You have two enormous financial goals and the quicker the better. That means you’re going to need options that will allow you to do both. So out comes Ramit Sethi’s Ladder or Personal Finance. It’s a gamechanger when it comes to building wealth and vanquishing debt. And here’s how it works:

The bottom lineLet’s face it, student loans are a drag. It’s only natural to want to get rid of them ASAP. But here’s the thing, we’re also getting older. Investing shouldn’t be relegated to some future date when things are peachy and the debts are done.

Do you know your earning potential?Take my earning potential quiz and get a custom report based on your unique strengths, and discover how to start making extra money — in as little as an hour. Should I Pay Off My Student Loans Or Invest? Here’s How To Decide is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/should-i-pay-off-my-student-loans-or.html October 27, 2021 at 10:34AM

What is a diversified portfolio? (with examples)

When it comes to building the best investment portfolio, you’ll often hear that diversification is key. But what does that even mean — and why do you need to bother with it? After all, you already own a wide range of stocks, from that skyrocketing Amazon stock to your Apple and eBay stocks, and you’re raking in the profits. What could go wrong? If you’re relying on a portfolio filled with big tech stocks or energy stocks to get you through to retirement — or if you’re banking on picking the right stocks forever — you may be in for a surprise during the next market downturn. It’s pretty easy to pick the “right” stocks with the market is overvalued. But, when a market correction happens, you’re probably going to be wishing you’d paid more attention to the advice about diversification. If you want to build wealth and make the right moves for your investments, you need to build a diversified portfolio.

What is diversification?Have you ever heard the saying, “Don’t put all your eggs in one basket?” That’s the same principle that drives investors to diversify their investments. When you diversify your investments, you spread your money out across different investment options to lower the risk that comes with investing. In other words, investors use diversification to avoid the huge losses that can happen by putting all of their eggs in one basket. For example, when you diversify, you allocate a portion of your investments to riskier stock market trading, which you spread out across different types of stocks and companies. When diversifying, you also put money into safer investments, like bonds or mutual funds, to help balance out your portfolio. The idea behind diversification is that you avoid relying on one type of investment or another. When one of your investments takes a tumble, the others act as a life raft for your money, providing solid returns until the riskier investments stabilize.

Bonus: Ready to learn more about investing? Download our FREE Ultimate Guide to Personal Finance.

Why is diversification important?A lack of diversification can cause big trouble for your money. That’s because:

Let’s say that you think tech stocks are the future. The tech industry is growing at a monumental pace, and you’ve been lucky with your tech stock purchases thus far. So, you take all of your investment money and you dump it into buying stock for large-cap tech company stocks. Now let’s say that the tech stocks have a steep uphill trajectory, making you tons of money on your investment. A few months later, though, bad news about the tech sector makes headlines, and it causes your cash-machine stocks to plunge, losing you tons of money in the process. What recourse do you have other than to sell at a loss or hold and hope they recover? Now, let’s say you invested heavily in large-cap tech stocks, but you also invested in small-cap energy stocks or medium-cap retail stocks, as well as some mutual funds, to balance it out. While the other types of investments have lower returns, they’re also consistent. When your sure-thing tech stocks take a nosedive, your safer investments help to protect you with ongoing returns, and you can better afford the losses from the riskier investments you made. That’s why diversification is important. It protects your money while letting you make riskier investments in hopes of bigger rewards. Diversification breakdown by ageDiversification is important at any age, but there are times when you can and should be riskier with what you invest in. In fact, most money experts encourage younger investors to focus heavily on riskier investments and then shift to less risky investments over time. The rule of thumb is that you should subtract your age from 100 to get the percentage of your portfolio that you should keep in stocks. That’s because the closer you get to retirement age, the less time you have to bounce back from stock dips. For example, when you’re 45, you should keep 65% of your portfolio in stocks. Here’s how that breaks down by decade:

Diversification vs. asset allocationWhile asset allocation and diversification are often referred to as the same thing, they aren’t. These two strategies both help investors to avoid huge losses within their portfolios, and they work in a similar fashion, but there is one big difference. Diversification focuses on investing in a number of different ways using the same asset class, while asset allocation focuses on investing across a wide range of asset classes to lessen the risk. When you diversify your portfolio, you focus on investing in just one asset class, like stocks, and you go deep within the class with your investments. That could mean investing in a range of stocks that have large-cap stocks, mid-cap stocks, small-cap stocks, and international stocks — and it could mean varying your investments across a range of different types of stocks, whether those are retail, tech, energy, or something else entirely — but the key here is that they’re all the same asset class: stocks. Asset allocation, on the other hand, means you invest your money across all categories or asset classes. Some money is put in stocks and some of your investment funds are put in bonds and cash — or another type of asset class. There are several types of asset classes, but the more common options include:

There are also alternative asset classes, which include:

When using an asset allocation strategy, the key is to choose the right balance of high- and low-risk asset classes to invest in and allocate the right percentage of your funds to lessen the risk and increase the reward. For example, as a 30-year-old investor, the rule of thumb says to invest 70% in riskier investments and 30% in safer investments to ensure you’re maximizing risk vs. reward. Well, you could allocate 70% of your investment to a mix of riskier investments, including stocks, REITs, international stocks, and emerging markets, spreading that 70% across all these types of asset classes. The other 30% should go to less risky investments, like bonds or mutual funds, to lessen the risk of losses. As with diversification, the reason this is done is that certain asset classes will perform differently depending on how they respond to market forces, so investors spread their investments across asset allocations to help protect their money from downturns.

Bonus: Ready to ditch debt, save money, and build real wealth? Download our FREE Ultimate Guide to Personal Finance.

Components of a well-diversified portfolioIn order to have a well-diversified portfolio, it’s important to have the right income-producing assets in the mix. The best portfolio diversification examples include: StocksStocks are an important component of a well-diversified portfolio. When you own stock, you own a part of the company. Stocks are considered riskier than other types of investments because they are volatile and can shrink very quickly. If the price of your stock drops, your investment could be worth less money than you paid if and when you decide to sell it. But, that risk can also pay off. Stocks also offer the opportunity for higher growth over the long term, which is why investors like them. While stocks are some of the riskiest investments, there are safer alternatives. For example, you can opt for mutual funds as part of your strategy. When you own shares in a mutual fund, you own shares in a company that buys shares in other companies, bonds, or other securities. The entire goal of a mutual fund is to lessen the risk of stock market investing, so these are typically safer than other investment types. BondsBonds are also used to create a well-diversified portfolio. When you buy a bond, you’re lending money in exchange for interest over a fixed amount of time. Bonds are typically considered safer and less volatile because they offer a fixed rate of return. And, they can act as a cushion against the ups and downs of the stock market. The downside is that the returns are lower, and are acquired over a longer-term. That said, there are options, like high-yield bonds and certain international bonds, that offer much higher yields, but they do come with more risk. CashCash is another component of a solid portfolio, and it includes liquid money and the money that you have in your checking and savings accounts, as well as certificates of deposit, or CDs, and savings and treasury bills. Cash is the least volatile asset class, but you pay for the safety of cash with lower returns. Additional components of diversificationThere are other components of diversification, too. As with the other asset classes, these alternative assets are used by some investors to further protect their portfolios. These include: Real estate or REITsYou can also use real estate funds, including real estate investment trusts (REITs), to diversify your portfolio and provide protection against the risks of other types of investments. Real estate funds work similarly to mutual funds, but rather than investing in a company that buys shares in bonds, stocks, and other common securities, you’re investing in a company that owns, operates, or finances income-generating real estate, like multi-unit apartments or rental properties. Asset allocation fundsAn asset allocation fund is a fund that is built to offer investors a diversified portfolio of investments that is spread across various asset classes. In other words, these funds are already diversified for investors, so they’re often the only fund necessary for investors to have a diversified portfolio. International stocksInvestors also have the option of investing in international stocks to diversify their portfolios. These stocks, issued by non-U.S. companies, can offer huge potential returns, but as with any other investment that offers the potential for a big payoff, they can also be extremely risky.

Bonus: Want to know how to make as much money as you want and live life on your terms? Download our FREE Ultimate Guide to Making Money

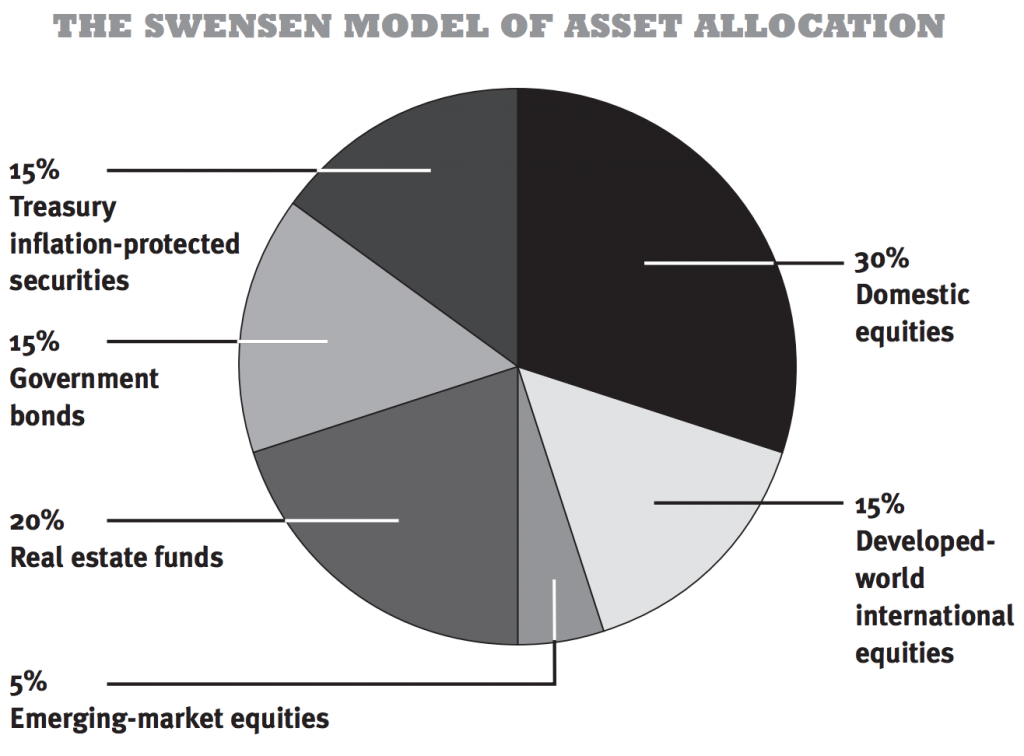

Diversified portfolio example #1: The Swensen Model

Just for fun, we want to show you David Swensen’s diversified portfolio. David runs Yale’s fabled endowment, and for more than 20 years he generated an astonishing 16.3% annualized return — while most managers can’t even beat 8%. That means he’s DOUBLED Yale’s money every four-and-a-half years from 1985 to today, and his portfolio is above. David is the Michael Jordan of asset allocation and spends all of his time tweaking 1% here and 1% there. You don’t need to do that. All you need to do is consider asset allocation and diversification in your own portfolio, and you’ll be way ahead of anyone trying to “pick stocks.” His excellent suggestion for how you can allocate your money:

What do you notice about this asset allocation? No single choice represents an overwhelming part of the portfolio. As illustrated by the tech bubble burst in 2001 and also the housing bubble burst of 2008, any sector can drop at any time. When it does, you don’t want it to drag your entire portfolio down with it. As we know, lower risk generally equals lower reward. BUT the coolest thing about asset allocation is that you can actually reduce risk while maintaining a solid return. This is why Swensen’s model is a great diversified portfolio example to base your portfolio on.

Bonus: Ready to start a business that boosts your income and flexibility, but not sure where to start? Download my Free List of 30 Proven Business Ideas to get started today (without even leaving your couch).

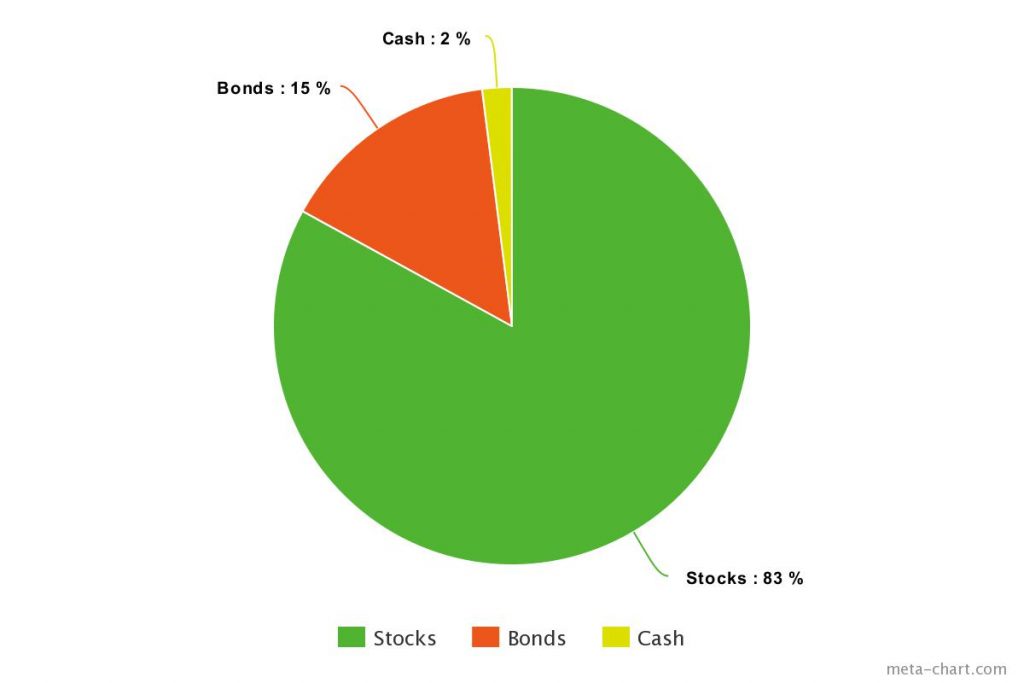

Diversified portfolio example #2: Ramit Sethi’s diversified portfolio example

This is our founder, personal finance expert Ramit Sethi’s investment portfolio. The asset classes are broken down like this:

Here are three pieces of context so you understand the WHY behind the numbers: Lifecycle funds: The foundation for my portfolioFor most people, Ramit recommend the majority of investments go in lifecycle funds (aka target-date funds). Remember: Asset allocation is everything. That’s why Ramit picks mostly target-date funds that automatically do the rebalancing for him. It’s a no-brainer for someone who:

They work by diversifying your investments for you based on your age. And, as you get older, target-date funds automatically adjust your asset allocation for you. Let’s look at an example: If you plan to retire in about 30 years, a good target date fund for you might be the Vanguard Target Retirement 2050 Fund (VFIFX). The 2050 represents the year in which you’ll likely retire. Since 2050 is still a ways away, this fund will contain more risky investments such as stocks. However, as it gets closer and closer to 2050, the fund will automatically adjust to contain safer investments such as bonds, because you’re getting closer to retirement age. These funds aren’t for everyone though. You might have a different level of risk or different goals. (At a certain point, you may want to choose individual index funds inside and outside of retirement accounts for tax advantages.) However, they are designed for people who don’t want to mess around with rebalancing their portfolio at all. For you, the ease of use that comes with lifecycle funds might outweigh the loss of returns. ConclusionAs an investor, it’s never wise to put all of your eggs in one basket. The key is to find the right strategy, whether that’s focusing on one asset category and going all-in on a wide range of investments within that category or spreading out your investments across all asset classes. Either type of investment strategy can help reduce the risk while increasing the possibilities of rewards, which is what investing is all about. Make sure you do your research and have the right approach for your needs, and you should be able to reap the benefits that a well-diversified portfolio offers. 100% privacy. No games, no B.S., no spam. When you sign up, we’ll keep you posted What is a diversified portfolio? (with examples) is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/what-is-diversified-portfolio-with.html October 27, 2021 at 10:34AM

Using a Roth Conversion Ladder to Retire Early

Many of us have dreamed of the potential of early retirement or FIRE, but it can be overwhelming to figure out how you might sustain yourself as you move into this new phase of your life. Luckily, there are many options. Aside from saving the amount you need to retire, you can also leverage several tax loopholes in order to acquire funds in your tax-advantaged investment accounts. One loophole: Build a Roth conversion ladder. A Roth conversion ladder works by converting money from a 401k to a Traditional IRA to a Roth IRA, and withdrawing the principal amount after five years without any penalties. This means you’ll be able to withdraw money from your 401k and Roth IRA earlier — allowing you to use your money faster and retire sooner (if that’s your thing). There is a bit more to it than that though. To fully understand how it works, we need to take a look at the issues with a Roth IRA on its own.

Having more than one stream of income can help you through tough economic times. Learn how to start earning money on the side with my FREE Ultimate Guide to Making Money

Roth IRAs and early retirementWhen considering early retirement, traditional IRAs and 401ks can seem to put you in an impossible situation. Don’t get us wrong. We love both of these forms of retirement savings, and they absolutely have their place on the journey of smart investing for retirement. Both of these accounts enable you to save for retirement in a highly productive way. A traditional IRA leverages your after-tax income to compound interest on your investments over time. You also don’t have to pay any taxes on it until after you withdraw it. The drawback? You can only withdraw your money once you reach retirement age. That means when you turn 59 1/2, you can finally get access to all that money, likely years after you would like if you are planning to retire early. Traditional IRA

401k

A 401k offers you similar gains and drawbacks to an IRA, giving you the chance to contribute pre-tax income this time which an employer can match. You still pay no taxes until you withdraw it at retirement age, but you also incur a penalty of 10% if you withdraw it before that age. This information can make some people feel like they are stuck between a rock and a hard place. But, luckily for you, this is where the Roth conversion ladder comes into play whether you have an IRA or a 401k.

Bonus: Unsure what the difference between a 401k and a Roth IRA is? Check out my Ultimate Guide to Personal Finance where I explain everything you need to know about retirement accounts.

What is a Roth Conversion Ladder?Simply put, a Roth conversion ladder is the loophole you have to withdraw a large pool of money from your retirement funds, both tax and penalty-free. Without this technique, anyone in the FIRE community will end up getting an early withdrawal penalty of up to 10%, taking quite a chunk out of those hard-earned savings. Most of those seeking early retirement do so because they have amassed a large amount of net worth. Their retirement investment accounts, such as a 401k or traditional IRA, will reflect this worth. For most of them, they plan to live on these investments for the rest of their life. The Roth conversion ladder allows them to access the accounts early in order to do that. The Roth conversion ladder essentially involves moving your money from your restrictive retirement accounts to more of an open system. Keep reading to figure out exactly how we recommend doing this. Who should use a Roth Conversion Ladder?A Roth conversion ladder is specifically useful for people who want to retire early. For example, if you plan to retire after you are 59 1/2, you will only lose out by transferring your money into a Roth IRA since it is no longer tax-protected. The positive aspect of the Roth conversion ladder is that it allows you to withdraw money to live in during early retirement. You should NOT use this method to supplement your income to achieve a lifestyle you can’t otherwise afford. Instead, the money should realistically stay in your retirement accounts to accrue as much tax-free interest for as many years as possible, or you will find retirement quite a challenge. How to set up your Roth Conversion LadderUtilizing a loophole to the penalty system in place around retirement funds might sound complicated. However, building an effective Roth conversion ladder is simply a matter of moving your money around and patience until it becomes usable. Start your Roth conversion ladder in just four steps.

The “ladder” part of the strategy comes into it when you use the technique on a recurring annual basis. As you move toward retirement, you continue to use the ladder to supplement your annual funds until you have reached five years before 59 1/2 when the funds become available. Why not just contribute annually to a Roth IRA?You take money out of a tax-protected account when you transfer money from a traditional IRA into a Roth IRA. That means you need to be ready to pay taxes on any money you transfer from a 401k or IRA into a Roth IRA. This is because contributions to a Roth IRA don’t lower your adjusted gross income, whereas you can get tax breaks when you make contributions to your 401k or traditional IRA. Instead, the money you transfer becomes taxable income for the year. Another reason you should avoid contributing to a Roth IRA annually is if you are getting anywhere close to emptying your retirement accounts before retirement age. You need to have enough saved to keep up your preferred lifestyle for as long as you plan to be in retirement. Additionally, you can only take money out of a Roth IRA five years after initially transferring the money into the account. You need to find some money to live on until then. You might already have this covered from There are plenty of ways to do that, though. Here are a few we at IWT love: Don’t forget about standard retirement accounts for early retirementSince your Roth conversion ladder only provides you money until you reach 59 ½ years old, you need to have a retirement savings plan for the years beyond that. The first step to finding out exactly how much you need for retirement, which you can do following the steps in the next section. However, when it comes to investing the money you save annually, you need to know what kinds of standard retirement accounts you should keep to make the most out of your money for early retirement? You will likely be saving a significant portion of your income each year for retirement, particularly if your goal is to do this early. However, it would be best to maximize your retirement accounts to make the journey faster. Although it will look different for anyone on the road to financial independence, the common accounts you can build while you are still working include:

Each of these works slightly differently and has various potentials of effectiveness for your retirement funds. So what do we mean by maxing these accounts out each month or year? All three of these accounts are tax-protected. The government caps the amount of investment in these so that those in a higher wage bracket don’t benefit more from tax breaks than most lower earners. Reaching these caps is your goal. From the time you build your net worth to your retirement goal, you are then ready to retire early and reap the rewards of these accounts using the Roth ladder strategy. Commonly asked questions about a Roth conversion ladderHow much money should I convert each year?The amount you should convert each year you employ the Roth ladder strategy depends on how much you have saved and how much you intend to spend each year. As long as you have enough saved for retirement, you should be able to send over the intended amount you will spend annually. So the real question is, how much should you save for retirement? You’ll need to look at three numbers to figure this out:

You might figure all these numbers out and then, six years later, experience a significant life change. Remember to be flexible with all of these, whether they go up or down. You never know what life has in store for you. Once you have calculated these numbers, you can come up with an annual savings rate for the precise amount you should be saving each month for your retirement. You can use this convenient calculator to figure it out. It utilizes the 4% Rule of a safe withdrawal rate. Do you not want the calculator to do the work for you? You can figure out your own 4% Rule number by:

The estimates below are all based on the expenses being multiplied by the typical 25 years assumed for a retiree.

Although the numbers might seem quite large, we are talking about what you need to save across a diversified portfolio of accounts over quite a few years. As long as you are willing to put the effort in and realize that the more you save, the earlier you can reach your retirement goals, you won’t have an issue hitting your goal numbers. How much should I expect to pay in taxes on a Roth IRA conversion?The exact number depends on the exact amount you transfer each year, tax percentages the year you transfer and inflation rates as time moves forward. However, the amount isn’t quite as important as the method you will use to pay that amount. Once you have figured out exactly how much you should expect to pay each time you move money from your 401k or IRA to a Roth, you need to be prepared to pay it. However, you shouldn’t have to worry too much about this since you will likely be living off the Roth contributions you made while working with a supplement of the money from your retirement funds. Moreover, since Roth contributions are already taxed, your tax bracket will only account for the yearly transfers and thus should be very low. Is there a limit I can convert into a Roth IRA?There is no limit to how much you can convert from your various retirement accounts into a Roth IRA. However, keep two things in mind. First, once that money leaves the tax-protected accounts, you will have to be ready to deal with the annual taxes. The second thing to remember is that a Roth ladder strategy only works as it should if you don’t run out of money. Therefore, it is essential to evaluate the long term to ensure you will still have the funds to continue supporting your lifestyle even after turning 59 1/2.

Saving for retirement is a habit you can build. Learn how to build good habits and break bad ones with our FREE Ultimate Guide to Habits.

What is the best time to start a Roth conversion ladder?When implementing a Roth conversion ladder, you should start your first Roth conversion the year you plan on retiring. After that, you should continue to make conversions for the annual amount you require to live each year, with conversion continuing up to 5 years before you turn 59 1/2. That way, the only financial “gap” you will have from your Roth conversion will be in the first five years of retirement. Once you reach 59 1/2, you can freely withdraw money from any of your retirement accounts. You can also do a Roth conversion after you have reached 59 1/2 years old. However, this kind of conversion always comes with a tax bill. While this is acceptable when the alternative is taking a 10% penalty fee that would come from withdrawing from your retirement accounts early, it isn’t necessary after you have reached retirement age. Additionally, when you move the funds out of your 401k or a traditional IRA, it means you will miss out on any tax-free growth you could have had. Playing your cards right during your working years can seem worthless if you have to take penalty fee after penalty fee to access your money. However, using a Roth conversion ladder gives you a way to join the FIRE community, enjoying early retirement without a 10% fee for it. If you are wondering how you might jump on this bandwagon of financial independence, check out our Ultimate Guide to Making Money so that you can start your own path to join the FIRE community. 100% privacy. No games, no B.S., no spam. When you sign up, we’ll keep you posted Using a Roth Conversion Ladder to Retire Early is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/using-roth-conversion-ladder-to-retire.html October 27, 2021 at 08:34AM

Informational interview questions to ask that create a lasting impression

What if you lost your job today and needed a new job in a week? Could you do it? What if you just wanted some advice for a tough career decision? Is there someone you could ask? Or what if you wanted to make a big career change, like switching industries? Is there anyone you could call for help? The secret to solving all of these challenges is the same: informational interviews.

Informational interviews: What they are and how they workYou’ve likely heard employment buzzwords like networking or mentoring being thrown around, but have you ever heard of the term informational interview? Informational interviews can be the difference between a thriving career and a career stalemate, but not everyone is familiar with how these types of interviews work. At a high-level, here’s how an informational interview works:

Simple, right? It is — as long as you understand the rules:

That said, informational interviews can most certainly lead to more job opportunities in the future, but only if you conduct them in the right way by asking the right questions to the right people. Let us show you how to master this powerful job search tool.

Bonus: Want to finally start getting paid what you’re worth? We show you exactly how in our Ultimate Guide to Getting a Raise and Boosting Your Salary

How to ask for an informational interview (and who to ask!)One of the biggest hurdles to getting an informational interview is knowing how to ask for one and who to ask. An informational interview is only useful if you target someone whose role you could see yourself in, whose field you may be interested in, or whose team you may want to be hired onto in the future. Otherwise, it’s just going to end up being coffee and a Q&A with no real purpose. While that’s nice, it’s not exactly the goal of the exercise. Before you send out any invites, though, be sure you know who exactly you need to interview. Here are a few tips to help narrow it down:

Once you’ve identified the person or persons you want to ask, all you have to do is reach out to the person you want to meet with by sending a friendly but concise email asking for a meeting. You’re free to word these requests as you see fit, but the wording of the email could be as simple as: “Hi, Brad! My name is Ann, and Kelly Smith suggested I speak with you because I am interested in learning more about your field or role. If you’re open to it, I would love to get some advice from you on this role or field. Would you have time in the next two weeks to meet for coffee so that I can learn more about your company and the role or field?” If you aren’t sure what to say, there are even word-for-word email scripts that can help. The hard work is basically done for you. You may strike out a few times, and that’s OK. Just keep reaching out to the right people, and eventually, you’ll find success.

Bonus: Want to work from home, control your schedule, and make more money? Download our FREE Ultimate Guide to Working from Home.

How to ask the right informational interview questionsOnce you’ve landed a “yes” for an informational interview, you need to take time to prepare for the interview, which starts with compiling a list of the right questions to ask. This step is crucial if you want to learn more about a role or company. It’s important to start the process of an informational interview with just one goal in mind: learning more about what the other person does and how they feel about it. These tips can help you ask the right types of questions:

These types of open-ended, well-phrased questions make the person you’re interviewing feel comfortable with you. They’re also a sign that you have respect for the other person’s experience and expertise, which is important if you want to also build a networking relationship. Here are a few examples you can use to help you craft your own questions: Example 1:

Example 2:

Example 3:

Notice the subtle differences? The good questions are open-ended and inquisitive. The not-so-good questions are pointed, closed questions that are going to make the person you’re interviewing very uncomfortable — and put your interview at risk of going downhill.

Bonus: Want to know how to make more money so you can live life on your terms? Download our FREE Ultimate Guide to Making Money

The big mistakes to avoid during informational interviewsKnowing who to ask for help — and what to ask — are just two small pieces of the informational interview puzzle. There is an art to pulling off a successful informational interview, and it involves a lot more don’ts than do’s. If you want to successfully navigate the art of informational interviews, you should make every effort to avoid the big (and surprisingly common) mistakes. These include: 1. Arriving late — or way too earlyIf you’re pursuing work- or career-related tips from your interviewee, chances are that they’re a busy professional with lots on their plate. What that means is that you should make every effort to avoid taking the other person’s time for granted. Don’t be late for your meeting — that’s an obvious one — but avoid being early, too, especially if you’re meeting at their place of employment. Don’t arrive more than five minutes early or you could put them in a precarious position (or embarrass yourself by barging in on a meeting you weren’t invited to). 2. Asking for a jobWhile you may want a job from this person. In fact, what they do may even be your dream job, but you need to avoid asking for a job opportunity at all costs. If you crafted your initial email the right way, you’ve already made it clear that you aren’t asking for anything other than the person’s time and insight. So, don’t flip the script on them when you meet in person. If you conduct yourself professionally and make a good impression, a job offer may organically grow from your interactions. But you are not there for a job interview, so don’t expect a job to grow out of your interactions. If it does? Great. If it doesn’t, you’ve still gained a lot of value from their time and insight. 3. Dominating the conversationIf you’re nervous, or if there are awkward pauses, you may feel tempted to try and fill the silence with nonstop chatter. Or, you may feel the need to offer commentary after every question is answered. Don’t do that. Ask and actively listen instead. Remember that the goal of this informational interview is to learn what you can from another professional who works in a job or at a company you’d like to pursue. You should be spending about 90% of your time during this interview on the listening end — not the talking end. If you’re finding yourself talking more than listening, you’re headed down the wrong path. 4. Asking for introductionsYou may have targeted your interviewee because they have great connections in the industry you want to be in. They may know the CEO of a certain company or have a friend or acquaintance who works in recruiting for a major firm. That’s all fine and good, but don’t allude to the fact that you’re looking for introductions to these key people. Keep the talk about the interviewee — not about who they know. And whatever you do, avoid asking for introductions to anyone on their connections list, in their current company, at their former company, or in their inner circle. You asked to meet with them to discuss their experience and role — not to meet another party who may benefit you more. 5. Skipping the thank youOne of the biggest mistakes people make is skipping the formal thank you after the informational interview. Remember that the person who met with you took time out of their busy schedule to try and help you. A sacrifice like that requires proper thanks. Send a card, an email, or some other form of written communication to thank them for the time they spent on you. Show them that you’re grateful for their help and advice, and do so quickly after you meet. This showcases your professionalism, and leaves them with the best impression of you possible — which can come in handy should future opportunities arise that you may be a fit for.

Bonus: Want to fire your boss and start your dream business? Download our FREE Ultimate Guide to Business.

One final informational interview tipWhile it’s important to have the right questions in mind and avoid the big mistakes when conducting an informational interview, you should also try not to overthink it. The goal of this process is for you to learn and grow while networking — not conduct every word, mannerism, and interaction by the book. That’s way too much pressure for one person to handle. But if you relax, engage, and most importantly, listen, you’re much more likely to come out of the process with the information that you need and a new networking contact on your side. If you’re too busy focusing on what to ask next or how to phrase the questions the right way, though, you’ll run the risk of missing vital information or advice — and that’s the opposite of what you want to achieve.

Do you know your earning potential?Take my earning potential quiz and get a custom report based on your unique strengths, and discover how to start making extra money — in as little as an hour. Informational interview questions to ask that create a lasting impression is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/informational-interview-questions-to.html October 27, 2021 at 08:34AM

How to Survive a Performance Improvement Plan

Being put on a Performance Improvement Plan (PIP) can feel like a kick to the gut, especially if it comes out of the blue and you don’t understand why. However, in most cases, it’s not a surprise. It usually comes after an employee has been struggling in their role or with some other issue at work. If you’re faced with a PIP and don’t know what to do, don’t panic! Below, you’ll learn how to survive and even thrive during a Performance Improvement Plan. For those who decide the job’s not right for them, there are also some bonus tips on how to find your dream job if this one doesn’t work out. Let’s get started on how to respond to a Performance Improvement Plan in the best ways possible.

What is a Performance Improvement Plan (PIP)?A PIP is a set of objectives given to an employee to help them develop in their role. It’s designed by employers to help their workforce better meet the responsibilities of the job. In a PIP, employers typically outline what needs to be improved in an employee’s skill set and experience. Later, the employee will be reassessed to see how they’ve improved. If you’re put on one, keep reading for some tips on how to survive a PIP. Why do managers use PIPs?Managers will create PIPs to help employees improve their work, boost efficiency, and that has a ripple effect across the rest of the business. It gives clarity to the employee as well because they know exactly what they need to do to improve and grow.

If poor work habits have landed you on a Performance Improvement Plan, it’s not too late. Learn how to build better habits and break bad ones with our FREE Ultimate Guide to Habits.

What to do if you’re put on a Performance Improvement PlanBeing put on a plan that tells you how much you need to improve can feel a little soul-crushing. You might be kept up all night thinking, “Am I going to get fired? Should I look for another job?” Honestly, maybe. It’s entirely possible that the performance review plan is only there to cover your boss legally before they boot you out the door. But before you panic, it’s also just as possible that your company is genuinely invested in you and hopes you hit your goals so they can keep you. Now, it goes without saying that it’s important to take your PIP seriously. There’s zero wiggle room for mistakes and not hitting the goals laid out. If you want to impress and keep your manager happy, here’s how to respond to a PIP. Don’t panicWhen you’re put on a PIP, panic might be your first response. You may be worried about losing your job, disappointing people, or appearing bad at your job. There are multiple reasons why someone might be put on a PIP. It might not all be down to you, and instead is about the company taking ownership as well. Focus on what you can do next and what you can control. It’s important that you react in a professional manner as your manager could be trying to gauge your reaction as well. A PIP doesn’t mean you’re going to be fired. In fact, it’s actually a good sign that the company wants to help you improve things. Rather than firing you outright, they want to help you develop in your role. So, try to look at it through a more positive lens … and take some deep breaths. Go in with a positive attitudeNo matter what your employer’s plan is or whether they have another agenda, you should remain calm and professional. Look at it as a way to develop your skills and improve yourself rather than a punishment. Your attitude will tell your employer a lot. If you are receptive to their suggestions, this is a good sign. If not, then they might think of alternatives that may involve hiring someone else. Ask for helpIf you know there are areas you’re a little less knowledgeable or experienced in, it’s time to reach out for help. Ask your manager, colleagues, or mentors for advice and guidance. If you’ve been put on a PIP, there are areas for improvement. So, try to set up weekly check-ins with your manager or ask for feedback from your boss. If you want to get ahead on this, be the first to suggest it. This will show you’re open and dedicated to improving. Take charge of your progressIf you’re committed to making progress, you need to own it and take the lead. Your manager may be in charge of drawing up the PIP, but it’s up to you to follow through. Make sure you take a close look through the plan and question anything that you need clearing up. Note, we said “question” not argue. You still need to stay on their good side. Take an active interest in everything being said and try to make suggestions of your own for how you can improve. Everyone could do something to improve, so find out what you could do. Admit it and be open about it. You could also make suggestions or ask about what the next steps are, whether they’re weekly check-ins or monthly one-to-ones. You want to show that you’re taking this seriously and are committed to progress. This will help ease any doubts the manager has about keeping you on the payroll. Identify the reasonsSomewhere along the way, something’s gone wrong. But it’s not always crystal clear what went wrong and when. When you first applied and got the job, you were qualified and experienced for it. So where’s the gap now? Did your job role change but you didn’t get any extra training? Have the manager’s expectations changed but there hasn’t been an open dialogue about it? Are there circumstances in your personal life affecting your work performance? Take some time to really dig into the reasons leading up to you getting a PIP. This isn’t about finger-pointing and seeing whose fault it is. It’s more about seeing the route cause and retracing your steps. That’ll help you and your managers come to a more informed decision about the next steps.

Bonus: Want to work from home, control your schedule, and make more money? Download our FREE Ultimate Guide to Working from Home.

Don’t go the extra mile – Go the extra inchNothing says “I’m taking this seriously” than doing just a little bit more than everyone else. We interviewed Pam Slim, author of Escape from Cubicle Nation, about how to become invaluable at your job. She told us a great story of how she went above and beyond to become amazing at her previous job. Here’s what she had to say: “I would get up really early in the morning and go sit with the traders on the floor. I would see what they did and proactively go to lunch with the most senior people who were great at giving financial advice, who were really like leaders in the industry. Because I was interested and because I, as the training and development director, wanted to really understand what they did to better serve their employees.” She went out of her way to take experts and co-workers to lunch to pick their brains, knowing she could learn information that would make her better at her job. This is a great tactic that we highly recommend. We also suggest checking out books and podcasts by industry leaders so you can learn from their years of experience. Keep in mind: Becoming great at your job doesn’t have to be drudgery. If you enjoy what you do, then learning how to do it better can be fun! Especially when you know it will make you invaluable to your company (and worth paying more.) A lot of the time, it’s simple acts like these that help you get ahead. Because guess what, most other people don’t bother. Taking the time to actively improve your knowledge and experience is exactly the kind of dedication and progress managers want to see. Answer questions before they’re askedImagine you’re at work. You think everything’s going great. But then your boss calls you into his office and starts in on everything you’ve done wrong. Total nightmare. To avoid this, do what top performers do. First, be proactive and keep your boss or manager updated with where your projects are at. Don’t wait for them to ask. If you know a question is coming soon, give them the answer before he can get the words out. For example, you can ask your supervisor if he’d like an “End of Day” report where you briefly tell him what you accomplished and what you have planned for tomorrow. It could look something like this:

An email like this lets your supervisor know you’re on track. Second, get in the habit of asking for feedback. Ask your boss how things are going from their perspective and what improvements they’d want to see from you. Asking for feedback may be uncomfortable at first, but it’s incredibly valuable. Constantly receiving and implementing feedback means you’re getting better at your job every day. This is a skill hiring managers are looking out for, and it’s surprisingly rare to find. It’s also a great way to show that you’re dedicated to improving things and managers love to see it, especially when they’ve drawn up a PIP. Look elsewhere if things don’t work outIf you’ve exhausted all of the above and things don’t seem to be improving, there’s another thing you can do -- look elsewhere. You might try your absolute best to rectify things with a PIP, but sometimes there’s only so much you can do. If the job is not the right fit for you, you can look elsewhere for a better fit. It’s still well worth trying to improve and progress in the meantime. It’ll keep your managers happy and it’s also good to leave on positive terms (especially if you need a referral). But don’t just go for any old job to replace this one. You could end up right back where you started. Instead, play it smart and develop a plan to find the right job for you next time. Keep reading for some simple pointers on how to do that… If your PIP doesn’t work out: How to find a job you loveSometimes it just doesn’t work out how we hope. Whether the blame rests on your shoulders, your manager’s, the company’s, or something else entirely, there’s no shame in walking away. Plenty of people take on jobs and realize months or years later that it’s just not a great fit. Everyone’s been through that at some point. If you decide that the job is not right for you and you’re likely to see another PIP or even disciplinary action in the future, it might be time to look elsewhere. Being put on a Performance Improvement Plan doesn’t make you a bad employee. It may be that this job isn’t the right fit for you. And you’re better off finding a job that challenges you and pays better. The problem is, very few people know how to find a job like that. People hop on Indeed or LinkedIn, fire off two dozen resumes in a weekend (to jobs we may not even want) then sit back and wait for a reply (which never comes). Top performers do things differently. They know how to find out exactly what job they want and what company they want to work for. They’ll even put out feelers to friends and co-workers to stay aware of what opportunities are out there. Top performers have much more clarity on what they want and how they can get there. It’s something that most people struggle with when it comes to the dreaded job hunt. Here’s an example from Judd W, an IWT reader, and graduate of the Dream Job program. “Last year I realized I wanted to switch industries. [IWT] helped me focus my search, network with insiders at the company I wanted to work with, take my interview skills to the next level, and, when the offer came in, negotiate what I was worth (over 20% more than the initial offer).” See? No wasting time on resumes or staring at the computer feeling lost. Judd followed a proven system for finding and landing a dream job and got tangible results. If you want a peek into the system top performers use to land dream job after dream job (even if you don’t have experience or a fancy degree), enter your name and email below. We’ll show you a special video on how top performers skip the front of the line and land a dream job that pays them 10%-50% more than they’re making now. And how you can follow that same system to find out what your dream job is, land it, and get paid what you’re worth. 100% privacy. No games, no B.S., no spam. When you sign up, we’ll keep you posted How to Survive a Performance Improvement Plan is a post from: I Will Teach You To Be Rich. Via Finance http://www.rssmix.com/via Blogger http://andrewburtonb.blogspot.com/2021/10/how-to-survive-performance-improvement.html October 27, 2021 at 08:34AM

Money Dials: The Reason You Spend the Way You Do According to Ramit Sethi

I always say, “Show me a person’s calendar and I’ll show you their priorities.” Well, I have a newer version of that: Show me a person’s spending, and I can show you what they love. I spent years talking to people about their spending habits, and I boiled them down to 10 “Money Dials.” They’re called Money Dials because you can “tune” them up or down — just like a dial. If you were to look at someone else’s spending for 10 minutes, you would instantly know what their Money Dial was. And if I were to look at your spending, I could tell you what yours is. Money Dials allow you to understand why people make the choices they do … and then go deeper than you ever thought possible. I find Money Dials fascinating for several reasons: People go where their time and money go. For example, fit people spend time and money to be fit. Fashionable people spend time and money reading fashion magazines and shopping. The most fascinating part is when we’re misaligned. For example, some people say, “Family is #1,” but if you look at their calendars and spending, family is not even in the top 10. Money Dials are an easy way to diagnose what you claim is important vs. what is actually important.

Ready to set up your finances to align with your Money Dials? Download my FREE Ultimate Guide to Personal Finance.

Every one of us has an area that we naturally love to spend money on. I’ve identified 10 Money Dials that we LOVE to pour our money into. If you look at your own spending, what gets you excited?

If you had $25,000 to spend on any of the above, which would you put your money into? Your answer — the one you instinctively came to within seconds — is likely your #1 Money Dial.

Want to know how to make as much money as you want and live life on your terms? Download my FREE Ultimate Guide to Making Money

Knowing your Money Dial can transform the way you think about your spending, because it lets you understand what you spend money on and why, and it enables you to redirect your spending from other areas to spend extravagantly on your Money Dial. THIS is what true Conscious Spending looks like. Money Dials are the evolution of Conscious Spending and zoom in on the concept of spending extravagantly — guilt-free. Below, I’m going to show you examples of people with different Money Dials. But the common theme is that whatever Money Dial a person chooses, they can build a life that allows them to spend extravagantly and unapologetically on the things that truly matter to them but also cut costs mercilessly on the things that don’t matter to them. This is the power of Money Dials. My favorite part of Money Dials is that once you understand your own, and you accept it, you can zoom in on what you love by TURNING THE DIAL ALL THE WAY UP. Finding your own Money DialsTo find your Money Dials, you just have to ask yourself one question: What do you LOVE to spend money on? That can be a deeply uncomfortable question to ask. It can actually be a little scary. Our culture and society love to demonize spending, especially when it comes to spending on ourselves. It comes with guilt, shame, and judgment. Don’t believe me? Here are some comments I’ve received on my various spending posts:

What a judgmental reaction — as if it’s forbidden and downright evil to spend on the things you love (and have the means to purchase). But what if we take these same judgmental people and examine their spending for a month? I bet I’d be able to find areas in their life where others would think they’re “wasting” their money too. It’s OK to recognize that you have areas you naturally love and want to spend on. What others think of your spending doesn’t matter because everyone has different Money Dials. It’s simply a matter of different priorities! In other words, what you value will be different from what others value. If you LOVE to spend your money on week-long trips to exotic locales, but someone else would rather spend that same amount of money on having the latest iPhone, that’s great — and perfectly normal! It’s just being true and honest to ourselves about what our Money Dials are. In fact, when we’re honest about acknowledging our Money Dials, we can adjust the dial (hence the term) as we need to be moderate, or turn them all the way up to spend even more on the things that bring us joy and more pleasant experiences (think splurging on first-class tickets instead of economy all the time, for example). This is crucial psychologically. Not only will we have more money and energy to spend on the things that bring us happiness, but we’ll be able to spend on those things guilt-free, since we know we’ve freed up the money by ignoring everything else. It’s intimidating and liberating at the same time. It allows us to say, “Hey, this is important to me — and that’s not.” The most successful people I’ve met are all very conscious about how they spend their money. That doesn’t mean they don’t spend at all. It means that they choose HOW and WHERE to spend their money, and are unapologetic in allocating significant resources to live a better life.

Want to work from home, control your schedule, and make more money? Download my FREE Ultimate Guide to Working from Home.

10 most common Money DialsDo you know what you naturally gravitate toward spending on? Most people don’t — even though everyone tends to have a few overriding priorities for their discretionary spending. When it comes to Money Dials, though, people’s spending almost always matches up with these 10 priorities.

I want to take a look at the four most common Money Dials. As you read, take note of how they fit into your spending habits. Here are the categories again:

Let’s take a look at what each of these Money Dials looks like. As you read, take note of how they fit into your own spending habits. Money Dial #1: ConvenienceThis Money Dial means spending on anything that makes your life more convenient. Examples:

I love spending my money on convenience. I’ve turned the Money Dial all the way up. I spend more than $50,000 a year on a personal trainer, chef, and other luxury services to streamline my life and reduce stress in those areas. And I also have a VA who: